Accounting Cycle, Fundamentals, Phases, and Advantages

Many businesses adhere to an eight-step accounting cycle to streamline financial management. This cycle concludes once transactions are recorded and incorporated into the year-end financial statements. This article covers the benefits, drawbacks, objectives, and stages of accounting for CA Exams .

What is Accounting Cycle?

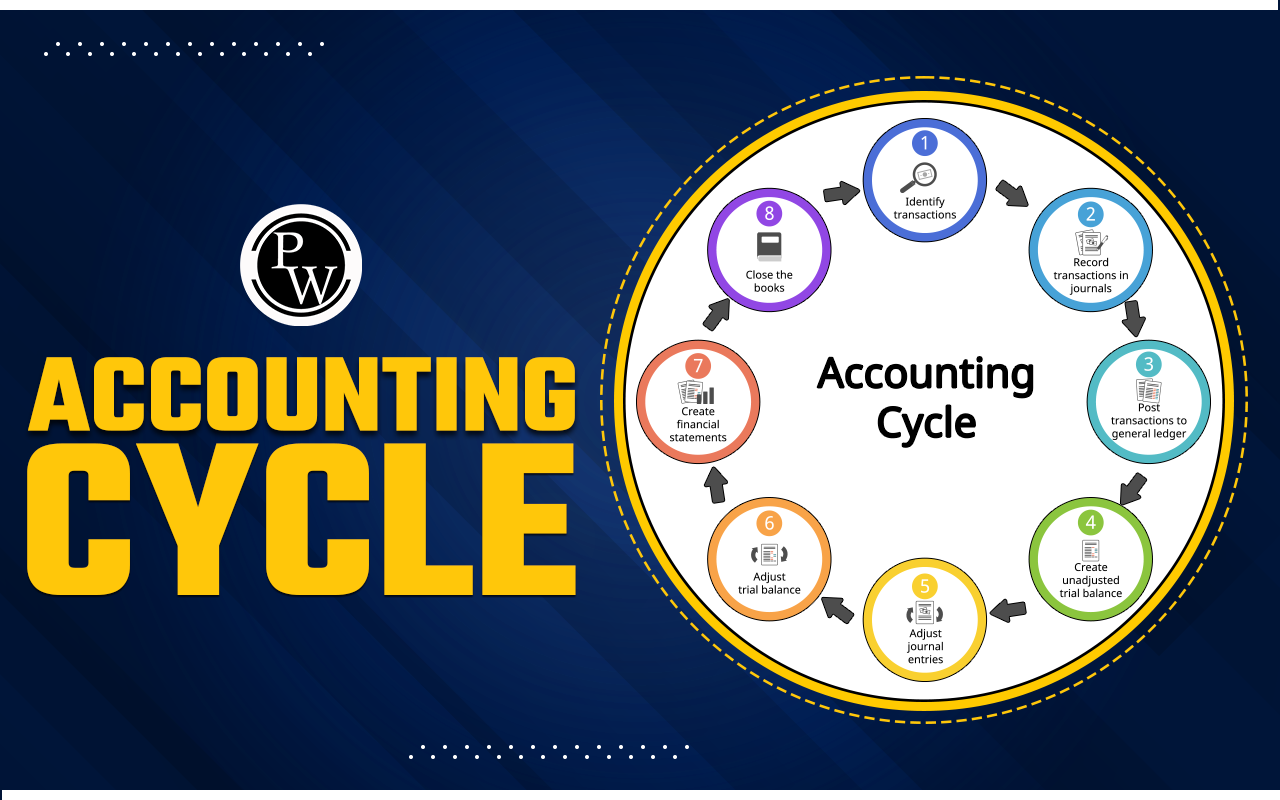

The accounting cycle encompasses the systematic process of identifying, examining, and documenting a company’s financial transactions. This structured eight-step method begins with transaction initiation and concludes with their inclusion in financial reports and record finalization. The accounting cycle is crucial for business owners as it simplifies financial accounting. It involves a series of steps to record, classify, and summarize financial information methodically. Starting when transactions occur, it concludes when these transactions are integrated into financial statements at the end of an accounting period. Nowadays, automation through various accounting software streamlines these steps, yet understanding the foundational phases of the accounting cycle remains essential.Fundamentals of Accounting Cycle

The accounting cycle is a step-by-step process that businesses use to keep track of their financial activities and create financial reports. This process ensures that everything is recorded accurately and follows accounting rules. Here are the main stages:Transaction Recognition: This is where businesses identify economic events like sales, purchases, and expenses that affect their finances.

Journal Entry: After identifying transactions, they are recorded in a journal. Each entry includes the date, accounts involved, amounts, and a brief description.

Posting to the Ledger: The information from the journal entries is transferred to the general ledger. This ledger organizes all accounts and shows changes in their values over time.

Initial Trial Balance: Once all transactions are recorded in the ledger, a trial balance is prepared. This lists all accounts and their balances to make sure the total debits equal the total credits.

Adjustments: Sometimes, not all financial events are recorded immediately. Adjustments are made at the end of the accounting period for things like depreciation of assets or unpaid expenses. These adjustments ensure that income and expenses are reported in the correct period.

Revised Trial Balance: After adjustments, another trial balance is prepared to ensure accuracy.

Financial Reports: Using the trial balance, businesses prepare important financial statements like the income statement (which shows profits and losses), the balance sheet (which shows assets and liabilities), and the cash flow statement (which shows cash inflows and outflows).

Closing Entries: At the end of the accounting period, temporary accounts like revenue and expenses are closed or transferred to a permanent account called Retained Earnings. This prepares the accounts for the next period.

Closing Trial Balance: This ensures that after closing entries, the total debits still equal the total credits, focusing on permanent accounts.

Reversing Entries: In some cases, adjustments made in one period need to be reversed in the next period to ensure accurate recording.

Also Check: Difference Between Accounting and Financial Management

Why Do Businesses Use Accounting Cycle?

Businesses rely on the accounting cycle for several key reasons:- It ensures accurate recording and preparation of financial statements.

- Facilitates the closure of books at the end of each accounting period.

- Provides essential data for financial statement analysis and effective business management.

Advantages of Accounting Cycle

Here are the benefits of implementing an accounting cycle:- Effectiveness Measurement: Businesses can assess the effectiveness of past financial strategies through the accounting cycle.

- Accurate Financial Statements: Following the accounting cycle ensures the generation of precise financial statements.

- Compliance: By adhering to established accounting principles and procedures within the cycle, businesses ensure compliance with accounting standards.

Disadvantages of Accounting Cycle

Here are the disadvantages of the accounting cycle:- Money Measurement Concept: Non-financial transactions are not recorded, which can lead to an incomplete portrayal of the company's overall situation.

- Limited Financial Insight: Omitting non-financial transactions means the full financial picture of the company may not be accurately represented.

- Impact of Accounting Methods: Accounting information can be influenced by various methods chosen by accountants, such as inventory valuation, depreciation methods, and how revenue and capital expenses are treated. This variability can affect the accuracy and comparability of financial data.

Phases of Accounting Cycle

The accounting cycle is a series of steps that businesses follow to record and analyze their financial transactions. These steps help business owners and accountants track the company's financial health accurately. Here’s a breakdown of each step:Identifying Transactions:

This step involves recognizing and documenting every financial transaction that occurs within the business. Whether it's a sale, purchase, or any other financial activity, it needs to be recorded in the company's books.Recording Transactions:

Once identified, transactions are recorded using a system called double-entry bookkeeping. This method ensures that every transaction affects at least two accounts, maintaining the balance between credits (money coming in) and debits (money going out).Posting:

After recording transactions in the general journal, they are posted or transferred to specific accounts in the general ledger. This ledger categorizes transactions by account type, like assets, liabilities, equity, revenue, and expenses.Trial Balance:

At regular intervals, usually at the end of each accounting period (like monthly or annually), accountants create a trial balance. This report lists all account balances to ensure that debits equal credits, highlighting any discrepancies that need correction.Worksheet Analysis:

A worksheet helps accountants make adjustments to ensure that financial statements accurately reflect the company's financial position. Adjustments may involve correcting errors or updating accounts to match actual income and expenses.Adjustments:

Adjusting entries are made to update account balances after the worksheet analysis. This step ensures that financial statements show the correct figures for revenues, expenses, assets, and liabilities.Generate Financial Statements:

Using the adjusted account balances, financial statements like the income statement (shows profits and losses), cash flow statement (tracks cash movements), and balance sheet (summarizes assets, liabilities, and equity) are prepared. These statements provide a clear picture of the company’s financial performance.Closing the Books:

At the end of the fiscal year, temporary accounts (like revenue and expense accounts) are closed out to start fresh for the next accounting period. This process involves ensuring all income and expense accounts have zero balances to begin anew.Post-Closing Trial Balance:

Finally, a post-closing trial balance confirms that all permanent accounts (like asset and liability accounts) have accurate balances after closing entries. This step ensures that the books are balanced and ready for the next accounting cycle. Join our PW CA courses today to master the accounting cycle and enhance your financial expertise. Gain practical skills for accurate financial reporting and strategic business management. Enroll now!| Also Check | |

| Public Finance and Budget | Inflation and Its Impact on Business |

| Common Accounting Mistakes | Economic Environment of Business |

| How to Read and Interpret Financial Statements? | GAAP vs. IFRS |

Accounting Cycle FAQs

What is the accounting cycle?

Why is the accounting cycle important for businesses?

What are the main stages of the accounting cycle?

How often does the accounting cycle occur?