E-Way Bill, Meaning, Requirements, Validity, Exemptions

With the introduction of the Goods and Services Tax (GST) in India, several compliance mechanisms have been put in place to ensure transparency in goods transportation. One of the most critical components of GST compliance is the E-Way Bill. This document is mandatory for the movement of goods beyond a certain threshold and plays a vital role in preventing tax evasion.

For CA exams, understanding the E-Way Bill is essential, as it directly impacts taxation, logistics, and compliance aspects of businesses.

What is an E-Way Bill?

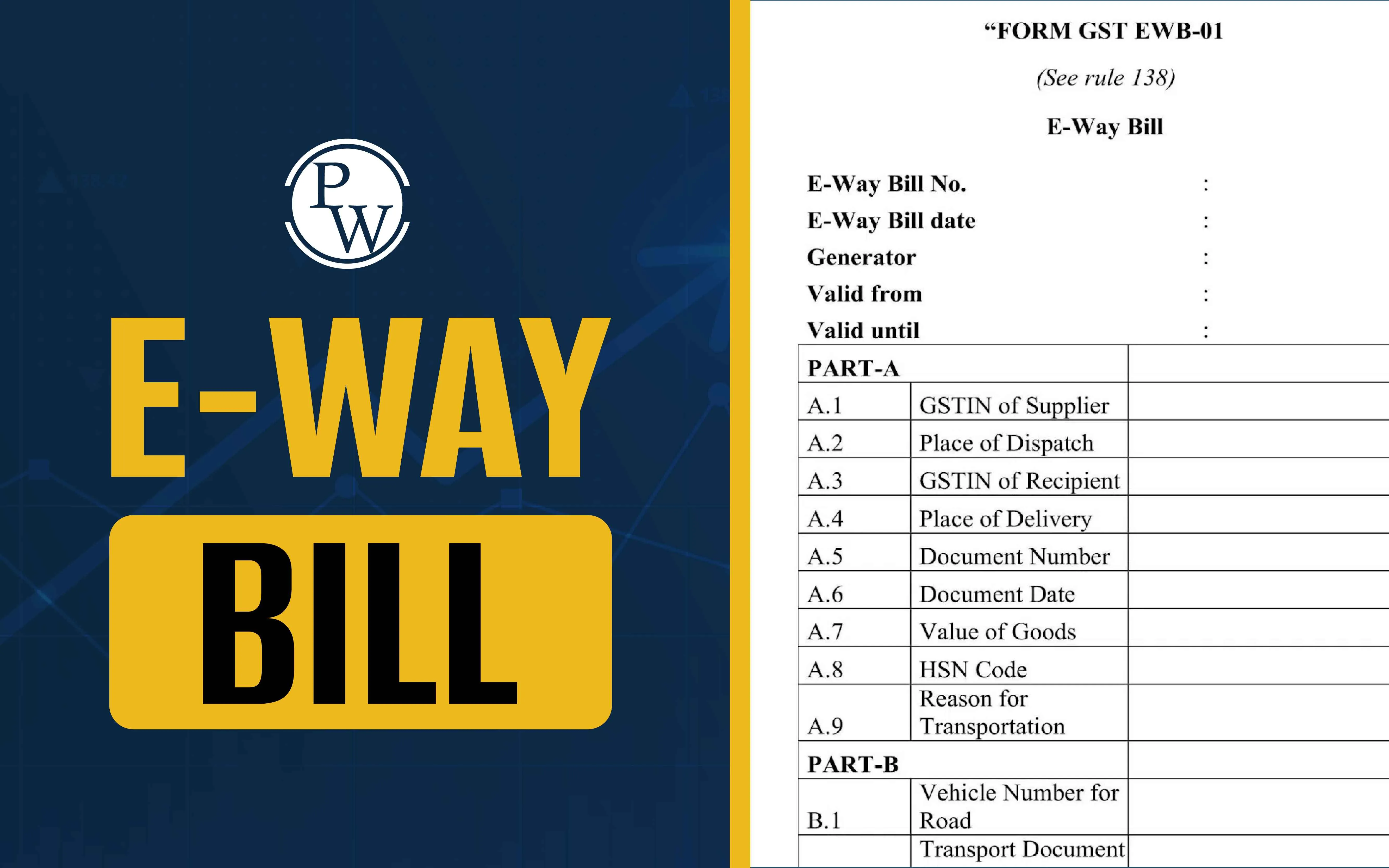

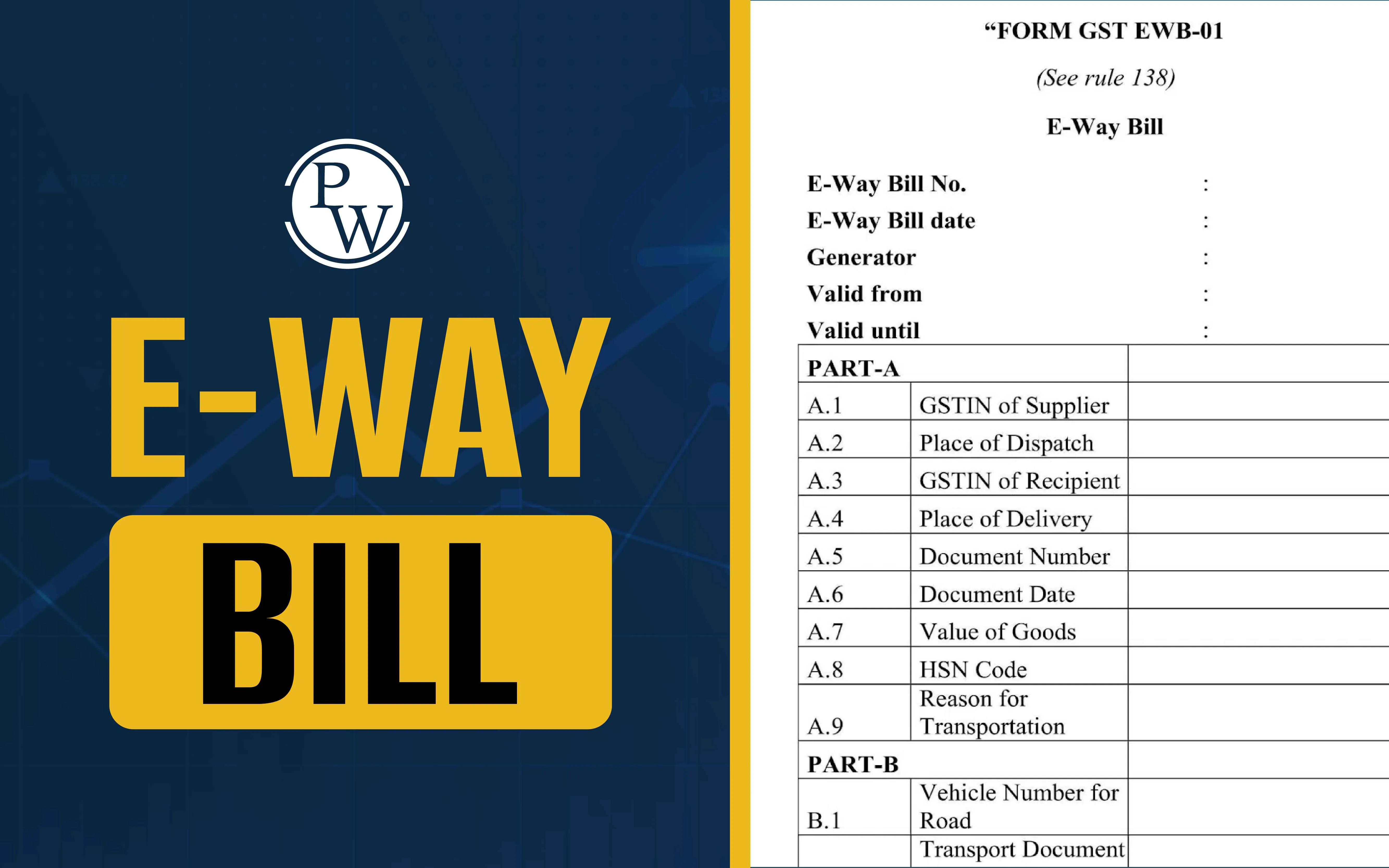

An E-Way Bill is an electronic document required for transporting goods valued at more than INR 50,000. It is generated online through the E-Way Bill portal (https://ewaybillgst.gov.in/), ensuring seamless tracking of goods movement. This document contains details of the consignment, such as:

- Invoice number and date

- GSTIN of the supplier and recipient

- Transporter details

- Description and value of goods

- Place of delivery and distance covered

Once generated, an E-Way Bill is assigned a unique E-Way Bill Number (EBN), which is used by suppliers, transporters, and recipients to track the shipment.

How is an E-Way Bill Generated?

The generation of an E-Way Bill is a crucial step in the GST compliance process. Businesses must ensure accuracy in entering transaction details to avoid errors. Below are the various methods for generating an E-Way Bill.

Online through the GST Portal

The E-Way Bill can be generated by logging into the official E-Way Bill portal. The user needs to navigate to 'Generate New' and enter transaction details, including invoice details, transporter ID, and vehicle number. Once the required information is provided, the request is submitted to generate a unique EBN.

SMS-Based Generation

To generate an E-Way Bill via SMS, the user must register a mobile number on the portal. A specific SMS code containing the required details is sent, and the E-Way Bill confirmation is received via SMS.

Mobile App or API Integration

Businesses with frequent transactions can automate E-Way Bill generation using API integration or the mobile app, making the process seamless and efficient.

Also Read: Steps to Conduct an Effective Risk Assessment

When is an E-Way Bill Required?

Understanding when an E-Way Bill is required is essential for ensuring compliance. The applicability of the E-Way Bill depends on the value of goods, mode of transport, and parties involved in the transaction.

Value Exceeds INR 50,000

An E-Way Bill must be generated when the value of goods being transported exceeds INR 50,000.

Registered vs. Unregistered Persons

If a registered supplier is transporting goods, they are responsible for generating the E-Way Bill. In cases where an unregistered supplier sells goods to a registered recipient, the recipient must generate the bill.

Transportation by Road, Rail, Air, or Ship

Regardless of the mode of transport, an E-Way Bill is required when the threshold value is crossed.

Interstate and Intrastate Movement

The requirement for an E-Way Bill applies to both interstate and intrastate transport, depending on state-specific rules.

Who Should Generate an E-Way Bill?

Determining responsibility for generating an E-Way Bill depends on the nature of the transaction. The following entities must ensure compliance with E-Way Bill regulations.

Registered Businesses

Registered businesses must generate an E-Way Bill when transporting goods exceeding INR 50,000. They may also generate an E-Way Bill voluntarily for lower-value transactions.

Unregistered Persons

If an unregistered person transports goods to a registered buyer, the recipient is responsible for compliance and must generate the E-Way Bill.

Transporters

If neither the supplier nor the recipient generates the E-Way Bill, the transporter must generate it before moving the goods.

Validity of an E-Way Bill

The validity of an E-Way Bill depends on the distance traveled:

- Standard goods: 1 day for every 200 km traveled.

- Over-dimensional cargo: 1 day for every 20 km traveled.

Validity can be extended eight hours before or after expiry to accommodate unforeseen delays.

When is an E-Way Bill Not Required?

There are scenarios where an E-Way Bill is exempted:

- Transportation by a non-motorized vehicle.

- Goods transported under customs supervision.

- Transit cargo to or from Nepal and Bhutan.

- Goods transported by government agencies.

- Goods moved within a 20 km radius for weighing purposes.

Documents Required for an E-Way Bill

To generate an E-Way Bill, businesses must have the following documents:

- Invoice, bill of supply, or delivery challan.

- Transporter ID, vehicle number, or transporter document details (for air, rail, or ship transport).

State-Wise E-Way Bill Rules

Each state may have specific rules regarding E-Way Bill thresholds. For example:

- Tamil Nadu: No E-Way Bill required for goods below INR 1,00,000.

- Delhi: Required for goods exceeding INR 1,00,000.

- Maharashtra: Mandatory for goods above INR 1,00,000.

Join PW CA Courses for guidance and structured study plans. Our courses provide insights into GST compliance, including E-Way Bill regulations, helping you in your CA journey!

| Also Check | |

| Business Accounting | Data Protection Laws |

| Inventories | Sustainable Economic Growth |

| Tax Implications of Mergers and Acquisitions | Difference Between Journal and Ledger |

GST Compliance FAQs

What is an E-Way Bill?

Who is responsible for generating an E-Way Bill?

How can I generate an E-Way Bill online?

What happens if an E-Way Bill expires before delivery?

Is an E-Way Bill required for all goods?