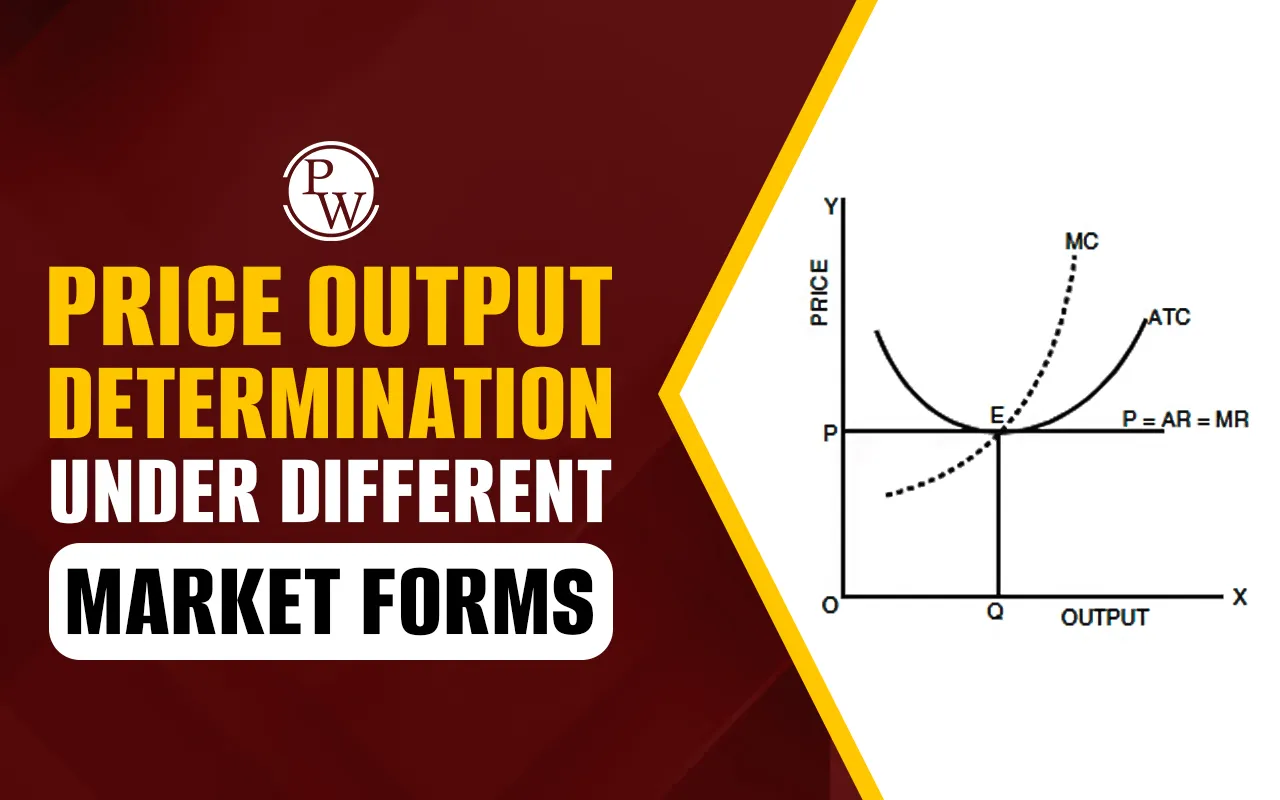

Price Output Determination Under Different Market Forms

Price plays a major role in every economic activity. Whether it's buying or selling, the price of a product or service directly influences the decision-making process. While buyers aim to get the best deal at the lowest cost, sellers aim to earn maximum profit. This is why understanding price determination is so important, it helps both parties reach a fair price based on market demand.

The forces of demand and supply play a key role in deciding the price of goods and services. These factors are also crucial in shaping a nation’s economy. For businesses, correct price determination supports better planning and profitability.

Price Determination is an important topic in the CA Exam. It is often asked in different formats, so having a clear understanding is essential. In this article, we’ll explore what price determination means, how it works in different market types, the key factors involved, and the step-by-step process behind it.

What is Price Determination?

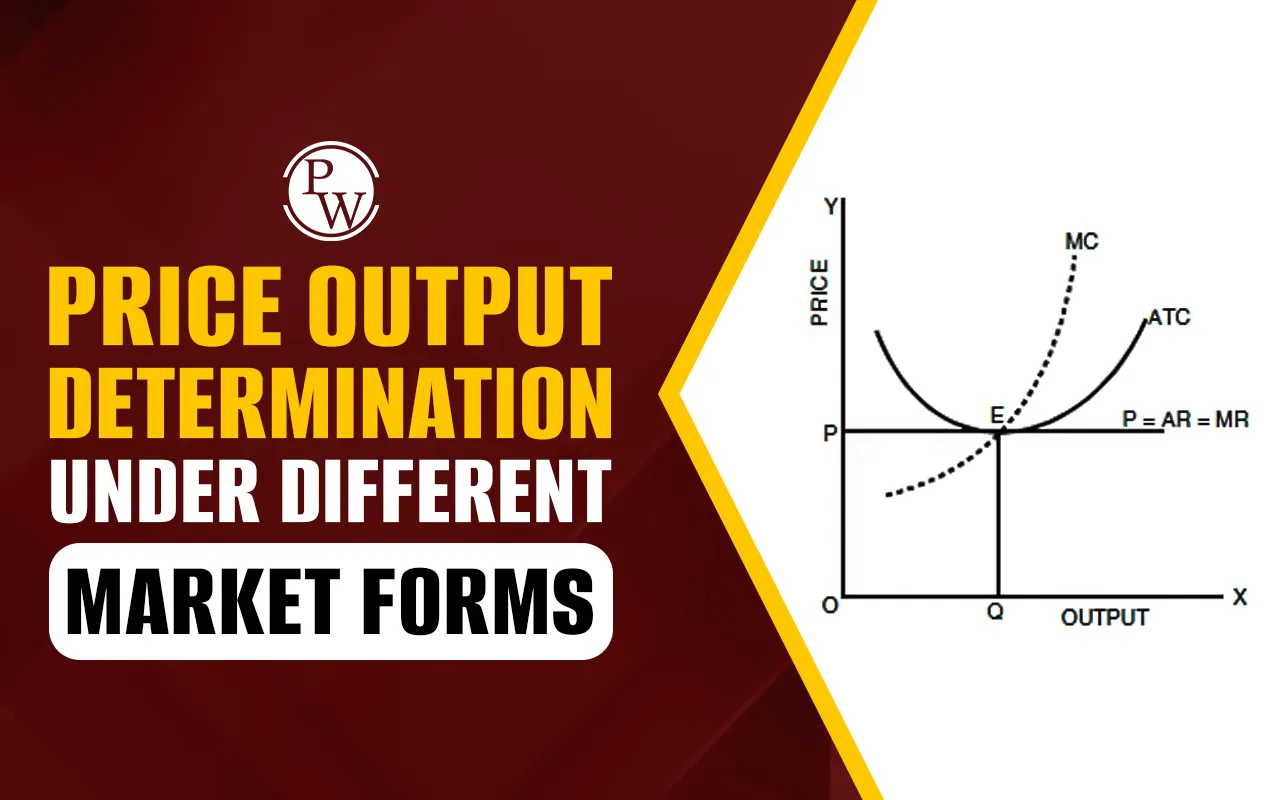

Price Determination refers to the process of deciding the cost of goods and services in a free market, where prices are not fixed by the government but are based on demand and supply.

In simple terms, demand means how many people want to buy a product or service, while supply refers to how much of that product is available for sale. In a free market, when more people want something (high demand) and it's in limited supply, the price goes up. On the other hand, if there’s a lot of that product available (high supply) but fewer buyers, the price drops.

This balance between demand and supply is what decides the final market price. The relationship is illustrated through demand and supply curves, showing how price and quantity are linked.

-

When prices are low, more people want to buy the product, demand increases.

-

When prices are high, fewer people want to, demand decreases.

-

If the price is low, sellers may not find it profitable to produce, supply decreases.

-

If the price is high, sellers produce more to earn more profit, supply increases.

So, demand and price move in opposite directions (inverse relationship), while supply and price move in the same direction (direct relationship).

Factors Influencing Price Determination

Several factors play a crucial role in determining the price of a product. Understanding these elements helps businesses set competitive and profitable prices.

Manufacturing Costs

The cost of producing a product includes both fixed and variable expenses. These costs, such as raw materials, labor, and salaries, must be covered to ensure profitability. If production costs are high, the product price will also be higher. Companies can manage variable costs effectively to maintain competitive pricing and boost demand, making it easier to control the overall pricing structure.

Market Competition

The level of competition in the market significantly impacts pricing. In a monopoly, where only a few companies dominate, new businesses must align their prices with existing competitors to attract customers. However, in markets with minimal competition, businesses can set higher prices without the fear of losing customers, as there are fewer alternatives available.

Product Utility

The perceived value or utility of a product also affects its price. Products that offer multiple benefits or fulfill various needs are less likely to be replaced by alternatives. The demand for such products often influences price determination as well. Even a small price change in competitive markets like FMCG can cause significant shifts in demand due to the availability of substitute products.

Pricing Objectives

Companies may have different goals that guide their pricing strategies. For instance, one company might aim to position itself as a premium brand, while another may focus on gaining market share. A premium brand may set higher prices to reflect superior quality, while a market-share-focused company might offer lower prices to attract customers quickly. The company’s specific objective plays a key role in setting the product price.

Government Regulations

In some industries, such as healthcare or essential services, government regulations can influence pricing. For example, the government may impose price caps on medicines or medical treatments to ensure accessibility for all. These regulations can restrict how companies set their prices in these regulated markets.

Marketing Costs

Marketing plays an essential role in the price-setting process. Companies that invest heavily in advertising, such as billboards or expensive campaigns, may increase the product price to cover these additional costs. This factor directly affects the final price that consumers see in the market.

These are the key factors influencing price determination that businesses must consider to set the right price while maintaining competitiveness and profitability.

Also Check: Differential and Integral Calculus in Business and Economics

Factors That Shift the Demand Curve

The demand curve shows how much of a product consumers are willing to buy at different prices. It slopes downwards, meaning when the price increases, demand usually falls, and when the price drops, demand rises.

However, the entire demand curve can shift based on various non-price factors. A rightward shift means an increase in demand, while a leftward shift indicates a drop in demand.

The following are the key factors that cause a shift in the demand curve:

1. Consumer Preferences

When consumer tastes change, like when a trendy product or new feature is introduced, it affects demand. If the product is liked, demand goes up (rightward shift); if not, demand falls (leftward shift).

2. Expectations About the Future

If people expect prices to rise soon, they tend to buy now, increasing current demand. If they expect prices to fall, they hold off, reducing current demand.

3. Consumer Income

A rise in income usually leads to an increase in demand, especially for branded or luxury items. On the other hand, a drop in income causes people to cut back on spending, reducing demand.

4. Substitute Products

When the price of a product rises, consumers may switch to its substitute. For example, if coffee becomes expensive, more people might start buying tea instead, increasing the demand for tea.

5. Complementary Products

These are goods used together, like mobile phones and chargers. If the price of phones goes up and fewer are bought, the demand for chargers also drops. So, a price change in one affects the other.

Factors That Shift the Supply Curve

The supply curve shows the relationship between a product’s price and the quantity producers are willing to supply. Unlike demand, supply has a direct relationship with price, higher prices lead to more supply, and lower prices lead to less.

The supply curve can also shift right (increase in supply) or shift left (decrease in supply) depending on several non-price factors.

The following are the key factors that cause a shift in the supply curve:

1. Manufacturing Costs

If raw material or labor costs go up, it becomes more expensive to produce goods. This reduces supply. But if costs go down, supply increases as production becomes more profitable.

2. Market Competition

When new sellers enter the market, the overall supply increases, often resulting in lower prices due to more options for buyers.

3. Government Policies

Taxes raise production costs and reduce supply, while subsidies help lower costs and boost supply. For instance, tax relief on solar panels can encourage manufacturers to produce more.

4. Technological Advancements

Better technology makes production faster and cheaper. This leads to an increase in supply as businesses can produce more at lower costs.

Process of Price Determination

Setting the right price is a major decision in any business. The process of price determination is all about finding a price that balances your costs, customer value, and business goals. Below is a step-by-step explanation that makes this process easier to understand.

Understanding the Market

The first step in determining price is to understand who your target customers are and what they need. At the same time, it’s important to study your competitors, how they price their products and what pricing strategies they use. This helps you find where your business fits in the market.

Calculating All Costs

Before you decide on any price, you need to calculate the total cost of making and selling your product or service. This includes the raw materials, labor, packaging, and delivery costs. You also need to consider indirect costs like rent, electricity, internet, and salaries of staff. Your price should always cover all your expenses.

Setting Profit Margin Goals

Once you know your costs, the next step is to set a target profit margin. This is the amount of profit you want to earn on each unit sold. By adding your desired profit to the cost, you get a base price that ensures your business remains profitable.

Analyzing Demand and Price Sensitivity

Understanding how your customers respond to price changes is very important. If a small change in price causes a big change in demand, your product is said to have elastic demand. If price changes don’t affect sales much, then demand is inelastic. Knowing this helps you decide how flexible your pricing should be.

Focusing on Customer Value

Rather than just focusing on costs, it's smart to price your product based on how valuable it is to your customers. If your product offers unique features, solves a problem, or saves time, customers may be willing to pay more. This value-based approach ensures you're not underpricing a high-quality offering.

Selecting the Right Pricing Strategy

Every business must choose a pricing strategy that fits its goals and brand. Some choose cost-plus pricing, where a fixed profit is added to the cost. Others follow competitors and set similar prices. Businesses entering new markets might use penetration pricing to attract customers. Premium pricing works for luxury items, while value-based pricing focuses on what customers think the product is worth.

Applying Psychological Pricing

Psychological pricing techniques influence buying decisions. For example, setting a price at ₹99 instead of ₹100 makes it feel more affordable, even though the difference is small. Offers, discounts, and limited-time deals also motivate customers to make a purchase sooner.

Testing Different Price Points

Before finalizing a price, it’s a good idea to experiment with different options. You can run A/B tests with two different price tags and see which one performs better. This helps you understand which price brings the most sales, revenue, or profit.

Making Price Adjustments

Pricing is not a one-time decision. Over time, market conditions change, customer preferences shift, and competitors take new actions. You should be ready to adjust your prices accordingly. Regular price adjustments help you stay competitive and profitable.

Following Legal and Ethical Rules

It’s important to ensure that your pricing methods follow local laws and ethical practices. Avoid tricks that mislead customers, such as hidden charges or fake discounts. Fair pricing builds trust and a positive brand image.

Communicating the Price Clearly

Once your price is set, communicate it in a clear and simple way across all marketing channels. Make sure your price reflects your brand image. For example, a premium brand should avoid appearing too cheap, while a value brand should avoid confusing pricing.

Reviewing and Improving the Pricing Strategy

The final step is to keep a close watch on your pricing strategy. Monitor customer feedback, sales performance, and competitor actions. If something isn’t working, don’t hesitate to change it. Regular reviews ensure your pricing remains effective and in line with your business goals.

| Also Check: | |

| Dissolution of Partnership Firm | Issue, Forfeiture and Re-Issue of Shares |

| LLP Accounts | Coding and Decoding |

| Retirement of a Partner | Social Accounting |

Price Output Determination FAQs

What is price determination?

How does demand affect price determination?

What factors influence price determination?

What is the relationship between supply and price?