Change in Supply, Meaning, Concept and Example

Change in Supply is essential for comprehending the dynamics of market economics. Checkout the article to learn more about change in supply and its definition, possibility and cause

Understanding the concept of "Change in Supply" is essential for comprehending the dynamics of market economics. In economic theory, supply refers to the quantity of a good or service that producers are willing and able to sell at different prices during a specific period. However, this quantity can fluctuate due to various factors affecting production capabilities and decisions made by suppliers.

A change in supply occurs when the quantity of goods or services supplied by producers shifts in response to alterations in factors other than price. These factors can include technological advancements, input costs, expectations of future prices, changes in the number of suppliers, and external shocks such as natural disasters or government policies. Each of these elements plays a critical role in influencing how much producers are willing to supply at any given price level.Fundamental Concept of Change In Supply

A change in supply refers to when producers of a particular good or service adjust their production levels or output. This adjustment can stem from technological advancements that enhance efficiency, reduce costs, or shift the number of competitors within the market. When there is a change in supply, it results in a shift in the supply curve. An increase in supply shifts the curve to the right, indicating that more of the product can be supplied at each price level. Conversely, a decrease in supply shifts the curve to the left, indicating a reduction in the quantity supplied at each price level. This shift prompts corresponding adjustments in market prices and demand to restore equilibrium. Economists commonly attribute changes in supply to several key factors:- Number of sellers in the market

- Expectations held by producers about future market conditions

- Prices of raw materials or inputs required for production

- Technological advancements influencing production processes

- Prices of other goods that producers could potentially produce instead

Supply and Demand Curves

Supply and demand curves are fundamental concepts in economics that illustrate the relationship between the price of a product and the quantity supplied or demanded in a market. Here’s an overview of each:Supply Curve:

The supply curve shows how much of a product or service suppliers are willing to produce and sell at different prices, holding all other factors constant. It is upward sloping from left to right, indicating that suppliers are motivated to produce more of the product as the price increases. Key features of the supply curve include:- Positive Slope: Higher prices incentivise suppliers to increase production due to higher profitability.

- Determinants: Factors influencing the supply curve include input costs, technology, expectations of future prices, number of sellers, and government policies.

- Shifts: Changes in these determinants can cause the supply curve to shift left (decrease in supply) or right (increase in supply), altering the quantity supplied at each price level.

Demand Curve:

The demand curve illustrates the quantity of a product or service consumers can purchase at different prices, assuming all other factors remain unchanged. It slopes downward from left to right, indicating that consumers typically demand more of the product as prices decrease. Key characteristics of the demand curve include:- Negative Slope: Lower prices attract more buyers, leading to higher demand.

- Determinants: Demand factors include consumer income, prices of related goods, tastes and preferences, population demographics, and expectations about future prices.

- Shifts: Changes in these factors cause the demand curve to shift left (decrease in demand) or right (increase in demand), affecting the quantity demanded at each price level.

Equilibrium:

The intersection of the supply and demand curves determines the market equilibrium, where the quantity supplied equals the quantity demanded at a particular price. Market forces ensure no excess supply or demand at equilibrium, thus stabilising the market price. Changes in either supply or demand disrupt this equilibrium, prompting price adjustments to restore balance. Understanding supply and demand curves provides insights into how markets function , how prices are determined, and how changes in economic conditions impact consumer and producer behaviour. These concepts are essential for analysing market dynamics and making informed economic decisions.| Also Read | |

| Short Run Supply Curve of a Firm | Demand Curve and the Law of Demand |

| Demand for Money – Meaning, Functions, Types | Supply Function- Meaning, Formula, Applications |

Possibility of Changes in Supply

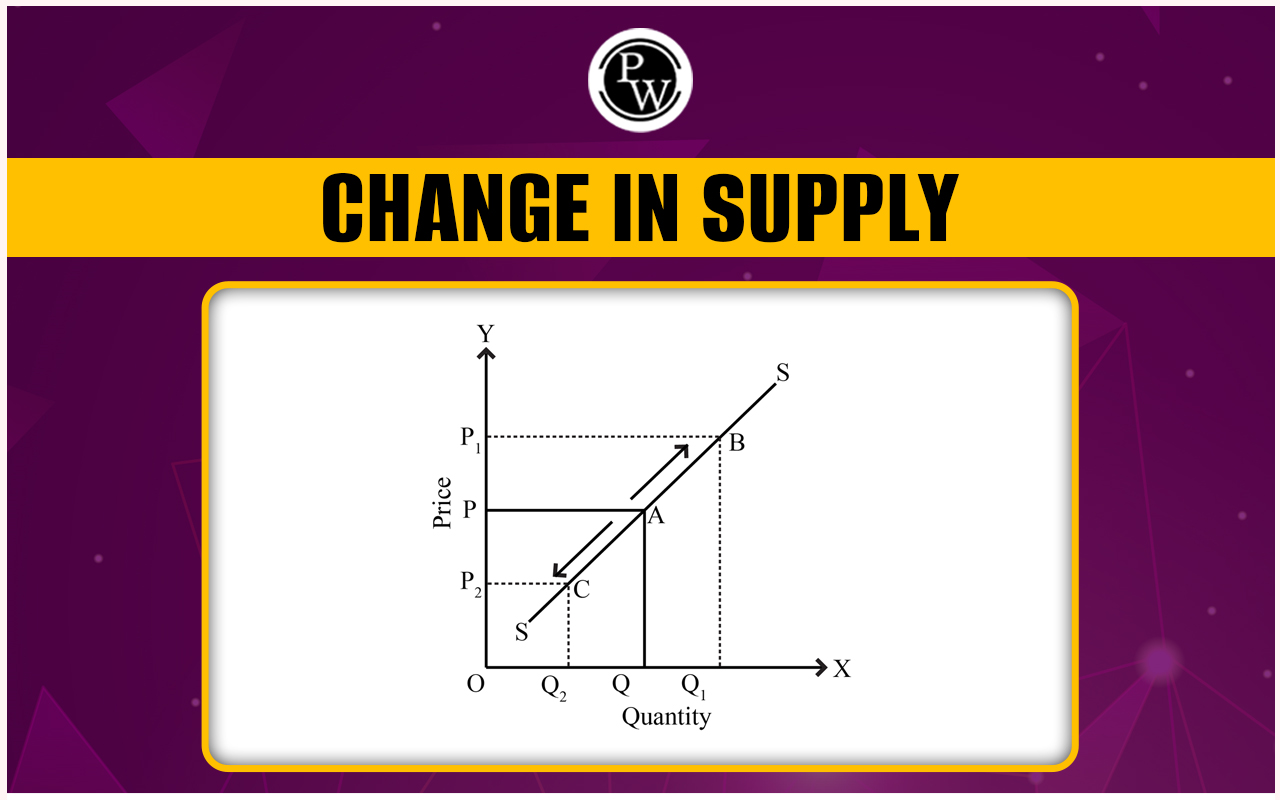

Change in supply refers to adjustments in the quantity of goods or services that suppliers are willing to produce and sell at various price levels in the market. This change can be influenced by technological advancements, input costs, or shifts in producer expectations. There are two scenarios for changes in supply:- Increase in Supply (Shift to the Right) : An increase in supply occurs when suppliers adopt new technologies that enhance production efficiency without affecting other factors. This leads to higher output at every price level. As a result, there is excess supply at the existing equilibrium price, prompting competition among suppliers to lower prices until a new equilibrium is reached. This results in a higher equilibrium quantity and a lower equilibrium price.

- Decrease in Supply (Shift to the Left ): Conversely, a decrease in supply happens when suppliers fail to adopt new technologies or face rising input costs, reducing their production capacity. This results in a lower quantity supplied at every price point. With decreased supply, there is excess demand at the original equilibrium price, causing prices to rise. This higher price attracts more suppliers into the market until a new equilibrium is established, characterised by a lower equilibrium quantity and a higher equilibrium price.

What Causes Change in Supply?

A change in supply refers to the alteration in the quantity of goods or services that suppliers are willing and able to offer at various price levels. Several factors can cause changes in supply:- Input Costs : Changes in the cost of production inputs such as labor, raw materials, energy, or technology can significantly impact supply. For instance, an increase in the price of raw materials reduces profitability, prompting suppliers to decrease production unless they can pass on the cost to consumers through higher prices.

- Technological Advancements : Innovations and technological advancements can improve production efficiency, reducing the cost of production and increasing supply. For example, adopting new machinery or production methods can allow suppliers to produce more output with the same resources.

- Government Policies : Government regulations, subsidies, taxes, or incentives can affect production costs and supply. Subsidies may lower costs for producers, thereby increasing supply, while taxes or regulations could increase costs, decreasing supply.

- Number of Sellers : The number of firms or sellers operating in a market can influence supply. More suppliers entering the market can increase overall supply, while exits or closures of firms can decrease supply.

Begin your journey towards academic excellence in Commerce with our comprehensive Commerce courses . Master the CBSE syllabus with expert guidance and ace your exams. Enroll now!”

Change in Supply FAQs

What is a change in supply?

A change in supply refers to the shift in the quantity of goods or services that producers are willing and able to supply at different prices during a specific period. This shift occurs due to factors other than price, such as technological advancements, input costs, expectations of future prices, changes in the number of suppliers, and external shocks like natural disasters or government policies.

How is a change in supply different from a change in quantity supplied?

A change in supply refers to a shift in the entire supply curve due to factors other than price. It indicates producers' willingness and ability to supply different quantities at each price level. In contrast, a change in quantity supplied is a movement along the supply curve caused solely by a change in the price of the goods or services. Quantity supplied increases as price rises and decreases as price falls, assuming all other factors affecting supply remain constant.

🔥 Trending Blogs

Join 15 Million students on the app today!

Free Learning Resources

PW Books

Notes (Class 10-12)

PW Study Materials

Notes (Class 6-9)

Ncert Solutions

Govt Exams

Our Other Websites

Class 6th to 12th Online Courses

Govt Job Exams Courses

UPSC Coaching

Defence Exam Coaching

Gate Exam Coaching

Other Exams

Know about Physics Wallah

Physics Wallah is an Indian edtech platform that provides accessible & comprehensive learning experiences to students from Class 6th to postgraduate level. We also provide extensive NCERT solutions, sample paper, NEET, JEE Mains, BITSAT previous year papers & more such resources to students. Physics Wallah also caters to over 3.5 million registered students and over 78 lakh+ Youtube subscribers with 4.8 rating on its app.

We Stand Out because

We provide students with intensive courses with India’s qualified & experienced faculties & mentors. PW strives to make the learning experience comprehensive and accessible for students of all sections of society. We believe in empowering every single student who couldn't dream of a good career in engineering and medical field earlier.

Our Key Focus Areas

Physics Wallah's main focus is to make the learning experience as economical as possible for all students. With our affordable courses like Lakshya, Udaan and Arjuna and many others, we have been able to provide a platform for lakhs of aspirants. From providing Chemistry, Maths, Physics formula to giving e-books of eminent authors like RD Sharma, RS Aggarwal and Lakhmir Singh, PW focuses on every single student's need for preparation.

What Makes Us Different

Physics Wallah strives to develop a comprehensive pedagogical structure for students, where they get a state-of-the-art learning experience with study material and resources. Apart from catering students preparing for JEE Mains and NEET, PW also provides study material for each state board like Uttar Pradesh, Bihar, and others

Copyright © 2026 Physicswallah Limited All rights reserved.