Capital Budgeting, Meaning and Techniques

Capital budgeting is the process of evaluating and deciding on long-term investment opportunities to allocate financial resources efficiently. Learn about capital rationing and risk assessment.

Capital budgeting is a process businesses use to assess potential major projects or investments. Examples of initiatives that usually require capital budgeting include constructing a new facility or acquiring a significant interest in an external venture. These evaluations help management decide whether to approve or reject such initiatives.

Meaning of Capital Budgeting

There are two types of expenditures generally made in a business viz. Capital Expenditure and Revenue Expenditure. Revenue expenditure is required for day-to-day operating requirements whereas Capital expenditure is incurred in investing in fixed assets.- Capital budgeting involves long-term planning and financing for proposed capital outlays (Horngren).

- It entails planning expenditures for assets whose returns will be realized in future periods (Spencer).

- Its aim is to maximize the long-term profitability of the firm by planning the development of available capital (Lynch).

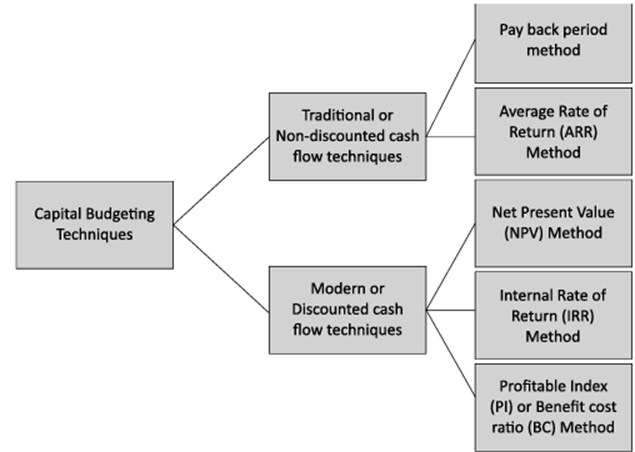

Capital Budgeting Techniques

1. Payback Period method

When someone invests money in any type of asset, they are often concerned about how long it will take to recoup their investment. This concern is shared by firms as well. When a company considers investing in a fixed asset, it looks for options that will return cash quickly. In this context, the payback period is a widely recognized and popular method of capital budgeting used to assess capital expenditure proposals. The payback period is defined as the amount of time required for the net cash inflows from an investment to cover the initial cost of the investment. The payback period is calculated as follows:- In the Case of Even Cash Inflows: If the cash inflows from an investment are consistent throughout its lifespan, the payback period can be calculated by dividing the investment cost by the annual cash inflow. As per formula:

- In the Case of Uneven Cash Inflows: If the cash inflows from an investment vary each year, the payback period is determined by summing the cumulative cash inflows for each year. The precise payback period can then be calculated using interpolation. Pay back period will be calculated as:PBP = E + B C Where, E = number of years immediately preceding the year of final recovery B = the balance amount still to be recovered C = cash flow during the year of final recovery

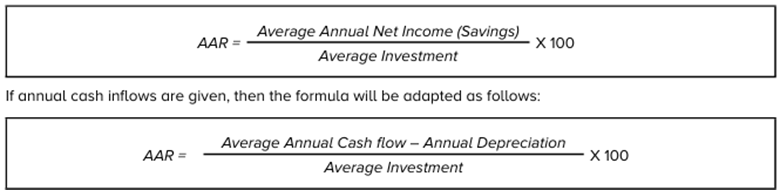

2. Average Rate of Return Method (ARR Method)

This method is also referred to as the unadjusted rate of return method or the Financial Statement Method because it primarily uses figures from accounting statements. In this approach, the percentage rate of return on the annual net profit from the investment is calculated. If based on the initial investment, it is known as Return on Investment (ROI); if based on the average investment, it is called the Average Rate of Return. Typically, it is calculated using the average investment in the project. When annual net income varies, the average annual net income is used in the calculation. Thus, the formula for calculating this return is as follows:

3. Present Value Method

The present value of future cash flows is found out with the help of the following algebraic formula: Present Value (P) = S /(1+i)n Where, P = Value of a future sum of money S = Future value of a sum of money i = Rate of interest n = number of years There are three methods of appraising the profitability of capital investment projects by present value technique:

- Net Present value Method (NPV Method) This method is also known as the Excess Present Value Method or Net Gain Method. It is used when management has set a minimum (or target) rate of return or cut-off rate. The steps involved in this method are as follows:(i) Determine the present value of all cash inflows from investments at different periods at required earnings rate. The formula is:Present value = Annual Cash Inflow x Present value Factor(ii) Calculate the present value of all cash outflows at different periods using the same earnings rate.

Cash outflows at the initial period (including the initial investment and any necessary working capital) are not discounted and have a present value factor of 1. However, cash outflows in subsequent periods are discounted using the appropriate present value factor. (iii) Determine the present value by comparing the total present value of all cash inflows with the total present value of all cash outflows. As per formula: Net Present value = Total Present value of Cash Inflows - Total Present value of Cash Outflows

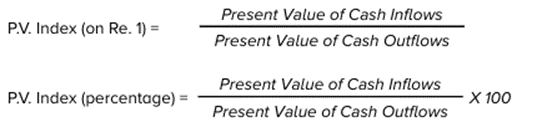

4. Profitability Index Method or Present value Index Method

The Profitability Index method, also known as the benefit-cost ratio, is a variation of the NPV method. It is favored over the NPV method when the capital costs of mutually exclusive projects vary significantly. This method quantifies the relationship between the present values of cash inflows and the present value of cash outflows (i.e., the investment cost). The formula is:

5. Time Adjusted Rate Of Return method (TAR Method) or Internal Rate Of Return Method (IRR Method)

This rate is also referred to as the 'Marginal Efficiency of Investment,' 'Internal Rate of Project,' and 'Break-even Rate.' It is derived from the discounted cash flow technique, which considers the time value of money, hence it's termed a time-adjusted rate. This approach is applied when management hasn't specified a preferred rate of return.Capital Rationing

Capital rationing is a method employed by companies to regulate their capital spending. It entails setting constraints on the amount of capital that can be invested during a specific timeframe, usually in line with financial resources or strategic goals. Companies may implement capital rationing through various means such as budget limits, confining investments to retained earnings, or utilizing hierarchical approval systems. This strategy might involve favouring smaller projects over larger ones to fully utilize the budget, potentially sacrificing optimal profitability. Consequently, capital rationing may not consistently produce the most advantageous results for the company. Types of capital rationing:- “hard” or external

- “soft” or internal

Risk and Uncertainty in Capital Budgeting

When assessing a proposal, the cash flows expected from an investment are projected, but the actual returns are only realized when the cash flow materializes. The uncertainty surrounding returns, from the time funds are invested until both management and investors ascertain the project's earnings, is a key factor determining the proposal's risk. Typically, owners of a company are apprehensive about the risk associated with their capital, prompting management to consider risk in evaluating capital budgeting proposals. Unlock your potential in corporate finance. Enroll in PW Company Secretary Courses today for expert guidance and excel in capital budgeting. Take the first step towards success!| Also Check: | |

| Introduction to Accounting | Capital Structure |

| Introduction to Accounting Standards | Introduction to Corporate Accounting |

| Law relating to Limitation | Law relating to Evidence |

Capital Budgeting FAQs

What is capital budgeting?

Capital budgeting is the process through which businesses evaluate potential major projects or investments to determine whether they should be pursued. It involves assessing long-term financial implications and risks associated with investing in fixed assets.

What are the main techniques of capital budgeting?

The main techniques of capital budgeting include the payback period method, average rate of return method (ARR), present value method (including net present value and profitability index methods), and the internal rate of return method (IRR).

How is the payback period calculated?

The payback period is calculated by dividing the initial investment cost by the annual cash inflow. If cash flows are uneven, the payback period is determined by summing the cumulative cash inflows until the initial investment is recovered.

What is the present value method in capital budgeting?

The present value method involves discounting future cash flows to their present value using a specified discount rate. It includes techniques like net present value (NPV), which compares the present value of cash inflows to the present value of cash outflows, and the profitability index, which assesses the ratio of present value of inflows to outflows.

What is capital rationing and its types?

Capital rationing is a method used by companies to regulate their capital spending. It involves setting constraints on the amount of capital that can be invested, either due to external factors (hard capital rationing) like creditor arrangements, or internal factors (soft capital rationing) like strategic goals or dividend policies.

Capital rationing is a method used by companies to regulate their capital spending. It involves setting constraints on the amount of capital that can be invested, either due to external factors (hard capital rationing) like creditor arrangements, or internal factors (soft capital rationing) like strategic goals or dividend policies.

Get Free Counselling Today

and Clear up all your Doubts

Talk to Our Counsellor just by filling out the form.

Join 15 Million students on the app today!

Free Learning Resources

PW Books

Notes (Class 10-12)

PW Study Materials

Notes (Class 6-9)

Ncert Solutions

Govt Exams

Our Other Websites

Class 6th to 12th Online Courses

Govt Job Exams Courses

UPSC Coaching

Defence Exam Coaching

Gate Exam Coaching

Other Exams

Know about Physics Wallah

Physics Wallah is an Indian edtech platform that provides accessible & comprehensive learning experiences to students from Class 6th to postgraduate level. We also provide extensive NCERT solutions, sample paper, NEET, JEE Mains, BITSAT previous year papers & more such resources to students. Physics Wallah also caters to over 3.5 million registered students and over 78 lakh+ Youtube subscribers with 4.8 rating on its app.

We Stand Out because

We provide students with intensive courses with India’s qualified & experienced faculties & mentors. PW strives to make the learning experience comprehensive and accessible for students of all sections of society. We believe in empowering every single student who couldn't dream of a good career in engineering and medical field earlier.

Our Key Focus Areas

Physics Wallah's main focus is to make the learning experience as economical as possible for all students. With our affordable courses like Lakshya, Udaan and Arjuna and many others, we have been able to provide a platform for lakhs of aspirants. From providing Chemistry, Maths, Physics formula to giving e-books of eminent authors like RD Sharma, RS Aggarwal and Lakhmir Singh, PW focuses on every single student's need for preparation.

What Makes Us Different

Physics Wallah strives to develop a comprehensive pedagogical structure for students, where they get a state-of-the-art learning experience with study material and resources. Apart from catering students preparing for JEE Mains and NEET, PW also provides study material for each state board like Uttar Pradesh, Bihar, and others

Copyright © 2026 Physicswallah Limited All rights reserved.