Introduction to Accounting Standards, Types of Entity

Accounting standards are rules for preparing and presenting financial statements consistently and transparently. Learn more about Accounting Standards in detail.

Accounting Standards are like official rules made by experts or government bodies. They cover how financial transactions should be recorded, measured, shown, and explained in financial statements. In this article, CS students will learn more about Accounting Standards for CS Exams.

What Are Accounting Standards?

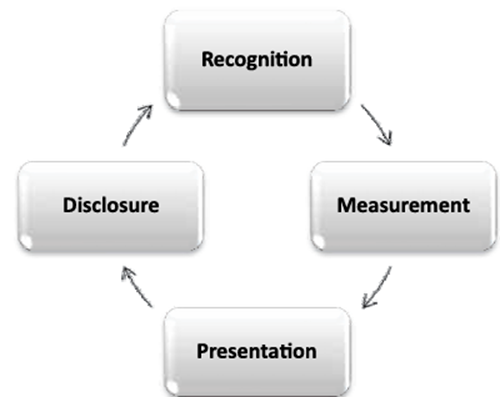

Accounting standards are a set of guidelines and rules used to ensure consistency, transparency, and accuracy in the financial reporting of businesses and organizations. These standards provide a framework for how financial statements should be prepared and presented, making it easier for stakeholders to understand and compare the financial performance of different entities.Recognition, Measurement, Presentation, and Disclosure

Accounting standards are like guidelines that show how to handle financial transactions. They explain how to recognize transactions, figure out their financial effect, show them in financial statements, and share important info with stakeholders. Following these steps makes sure that the financial info truly represents what's happening in a business.

Accounting standards are like guidelines that show how to handle financial transactions. They explain how to recognize transactions, figure out their financial effect, show them in financial statements, and share important info with stakeholders. Following these steps makes sure that the financial info truly represents what's happening in a business.

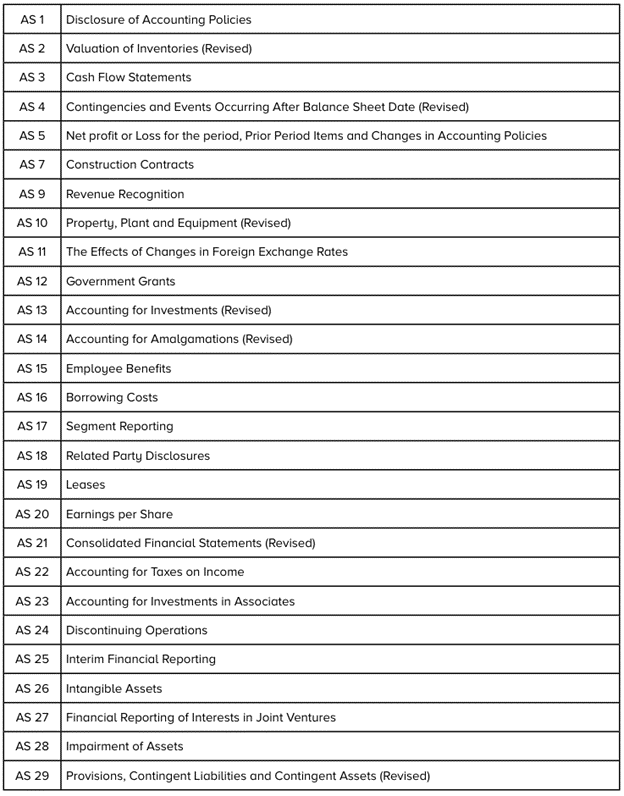

List of Accounting Standards by ICAI

List of Accounting Standards by ICAI is given in the table below:

Applicability of Accounting Standards

Accounting standards ensure uniformity, transparency, and reliability in financial reporting across various entities. Here is an overview of the applicability of accounting standards to different types of entities: (a) Sole proprietorship concerns/individuals (b) Partnership firms (c) Societies (d) Trusts (e) Hindu Undivided families (f) Association of Persons (AOP) (g) Body of individuals (BOI) (h) Co-operative societies (i) Companies and LLPsTypes of Entity

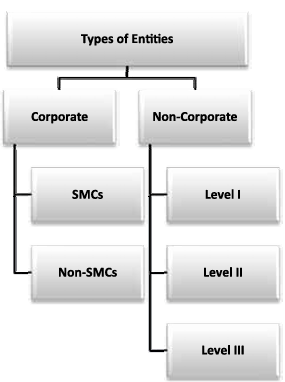

There are two main types of entities i.e. corporate and non-corporate. Check the types of entities in the image below:

Corporate Entities

Check the details about Corporate Entities in the table below:| Corporate Entities | ||

| Type | Conditions | Applicability of Accounting Standard |

| Small and Medium Companies (SMCs) | SMCs are companies that satisfy the following conditions: (a) Equity and debt securities of the company are not listed or are not in the process of listing on any stock exchange, whether in India or outside India (b) Company is not a bank or financial institution or insurance company (c) Company’s turnover (excluding other income) does not exceed Rs. 50 crores in the immediately preceding accounting year (d) Company does not have borrowing (including public deposits) exceeding Rs. 10 crores at any time during the immediately preceding accounting year and (e) Company is not a holding company or subsidiary of a non-SMC. | Partial Exemption: Certain relaxations are provided with respect to following Accounting Standard: AS 17 – Segment Reporting AS 15 – Employee Benefits AS 19 – Leases AS 20 – Earnings Per Share (EPS) AS 29 – Provisions, contingent liabilities and contingent assets Full Exemption AS 3 – Cash Flow Statements, shall not apply to SMCs if it is a One Person Company (OPC), dormant company and Small Company |

| Non-SMCs | Any Other Corporate Entities not falling under SMCs | All the accounting standards are applicable to Non-SMCs. |

Non-corporate Entities

Check the details about Corporate Entities in the table below:| Non-Corporate Entities | ||

| Level | Conditions | Accounting Standards applicable |

| Level I | 1.Entities whose equity or debt instruments are listed or are in process of listing on any stock exchange (in or outside India) 2.Banks (including co-operative banks), financial institutions or entities carrying on Insurance business 3. All commercial, industrial or business reporting entities having: – Borrowings > 10 crores (at any time during immediately preceding accounting year) – Turnover > 50 crores (during preceding accounting year) l Holding or subsidiary entities of any of the above. | All the accounting standards are applicable to Level I entities. However, AS 21, 23 and 27 will apply based on regulatory requirements. |

| Level II | Other than Level I entities if they fall under the following limit. All commercial, industrial or business reporting entities having: – Borrowings > 1 crores (at any time during immediately preceding accounting year) – Turnover > 10 crores (during preceding accounting year) Holding or subsidiary entities of any of the above. | Fully applicable AS All accounting standards are applicable to Level II entities except AS 21, 23, 25, 27 and those discussed below. |

| AS applicable but certain relaxations regarding disclosure requirement AS 19 – Leases AS 20 – Earning Per Share AS 29 – Provisions, contingent liabilities and contingent assets. | ||

| Accounting standards not applicable AS 3 – Cash Flow Statement AS 17 – Segment Reporting. | ||

| Level III | All non-corporate entities other than Level I and Level II. | In addition to partial and full exemption as given in Level II, full exemption with respect to these two are also available: AS 18 – Related Party Disclosures AS 24 – Discontinuing Operations. |

International Financial Reporting Standards (IFRS) as Global Standards

IFRS has become the worldwide standard for financial reporting. It helps make financial statements consistent and easy to compare between different countries. Using IFRS makes international trade, investment, and deciding where to put money easier.Convergence of Accounting Standards with IFRS in India

India has been aligning its accounting standards with IFRS to enhance transparency and facilitate global integration. This convergence process aims to bridge the gap between Indian Generally Accepted Accounting Principles (GAAP) and international standards.List of IFRS and Indian Accounting Standards (Ind AS)

The following are the list of IFRS and Indian Accounting Standards (Ind AS):- IFRS 1-First time Adoption of International Financial Reporting Standards

- IFRS 2-Share Based Payments

- IFRS 3-Business Combinations

- IFRS 4-Insurance Contracts

- IFRS 5-Non-current Assets Held for Sale and Discontinued operations

- IFRS 6-Exploration for and Evaluation of Mineral Resources

- IFRS 7-Financial Instruments: Disclosures

- IFRS 8-Operating Segments

- IFRS 9-Financial Instruments

- IFRS 10-Consolidated Financial Statements

- IFRS 11-Joint Arrangements

- IFRS 12-Disclosure of Interests in other Entities

- IFRS 13-Fair Value Measurement

- IFRS 14-Regulatory Deferral Accounts

- IFRS 15-Revenue from Contracts with Customers

- IFRS 16-Leases

- IAS-1-Presentation of Financial Statements

- IAS-2- Inventories

- IAS-7- Statement of Cash Flows

- IAS-8- Accounting Policies, Change in Accounting estimates and Errors

- IAS-10- Events after balance sheet date

- IAS-12- Income Taxes

- IAS-16-Property, Plant and Equipments

- IAS-19- Employee Benefits

- IAs-20-Accounting for Govt. Grant and Disclosure of Govt. Assistance

- IAS-21- The Effect of Changes in Forex Rates

- IAS-23-BorrowingCosts

- IAS-24- Related Party Disclosures

- IAS-26- Accounting and reporting by retirement benefit plans

- IAS-27- Separate Financial Statements

- IAS-28- Investment in Associates and Joint Ventures

- IAS-29- Financial Reporting in Hyper inflationary Conditions

- IAS-32- Financial Instruments- Presentation

- IAS-33- Earnings Per Share

- IAS-34- Interim Financial Reporting

- IAS-36- Impairment of Assets

- IAS-37- Provisions, Contingent Liabilities and Contingent Assets

- IAS-38- Intangible Assets

- IAS-40-Investment Property

- IAS-41-Agriculture

IFRS vs. Indian GAAP

Comparing IFRS with Indian GAAP highlights the differences in accounting principles, treatment of transactions, and disclosure requirements. Understanding these variances is crucial for businesses transitioning to Ind AS and complying with global reporting standards.Comparison of Indian GAAP and Ind AS

A comprehensive comparison between Indian GAAP and Ind AS elucidates the changes in accounting treatments, financial statement presentation, and disclosure requirements. This analysis aids businesses in navigating the transition smoothly.| Also Check: | |

| Introduction to Accounting | Capital Structure |

| Law relating to Civil Procedure | Right To Information Act, 2005 |

| Law relating to Limitation | Law relating to Evidence |

Accounting Standards FAQs

What are accounting standards?

Accounting standards are a set of guidelines and rules used to ensure consistency, transparency, and accuracy in the financial reporting of businesses and organizations.

Why are accounting standards important for businesses?

Accounting standards ensure that financial statements are consistent and comparable, which helps stakeholders make informed decisions, enhances transparency, and maintains reliability in financial reporting.

Do sole proprietorships and partnerships need to follow accounting standards?

Sole proprietorships and partnerships are generally not required to follow mandatory accounting standards, but adhering to basic accounting principles is recommended for accurate financial reporting and tax purposes.

How do accounting standards apply to companies and LLPs?

Companies and LLPs must follow mandatory accounting standards, such as IFRS or local GAAP, to ensure compliance with regulatory requirements and provide transparent financial information to stakeholders.

What is the difference between Indian GAAP and Ind AS?

Indian GAAP and Ind AS differ in accounting principles, treatment of transactions, and disclosure requirements. Ind AS is aligned with IFRS, aiming to bring Indian financial reporting in line with global standards.

Talk to a counsellorHave doubts? Our support team will be happy to assist you!

Get Free Counselling Today

and Clear up all your Doubts

Talk to Our Counsellor just by filling out the form.

Join 15 Million students on the app today!

Free Learning Resources

PW Books

Notes (Class 10-12)

PW Study Materials

Notes (Class 6-9)

Ncert Solutions

Govt Exams

Our Other Websites

Class 6th to 12th Online Courses

Govt Job Exams Courses

UPSC Coaching

Defence Exam Coaching

Gate Exam Coaching

Other Exams

Know about Physics Wallah

Physics Wallah is an Indian edtech platform that provides accessible & comprehensive learning experiences to students from Class 6th to postgraduate level. We also provide extensive NCERT solutions, sample paper, NEET, JEE Mains, BITSAT previous year papers & more such resources to students. Physics Wallah also caters to over 3.5 million registered students and over 78 lakh+ Youtube subscribers with 4.8 rating on its app.

We Stand Out because

We provide students with intensive courses with India’s qualified & experienced faculties & mentors. PW strives to make the learning experience comprehensive and accessible for students of all sections of society. We believe in empowering every single student who couldn't dream of a good career in engineering and medical field earlier.

Our Key Focus Areas

Physics Wallah's main focus is to make the learning experience as economical as possible for all students. With our affordable courses like Lakshya, Udaan and Arjuna and many others, we have been able to provide a platform for lakhs of aspirants. From providing Chemistry, Maths, Physics formula to giving e-books of eminent authors like RD Sharma, RS Aggarwal and Lakhmir Singh, PW focuses on every single student's need for preparation.

What Makes Us Different

Physics Wallah strives to develop a comprehensive pedagogical structure for students, where they get a state-of-the-art learning experience with study material and resources. Apart from catering students preparing for JEE Mains and NEET, PW also provides study material for each state board like Uttar Pradesh, Bihar, and others

Copyright © 2026 Physicswallah Limited All rights reserved.