Types of Banks in India: Public, Private, RRB, Co-operative, Small Finance Explained

India's banking system is vast and can seem confusing at first. If you are a student preparing for exams or just curious about money matters, knowing the types of banks in India will help you understand how the whole system works.

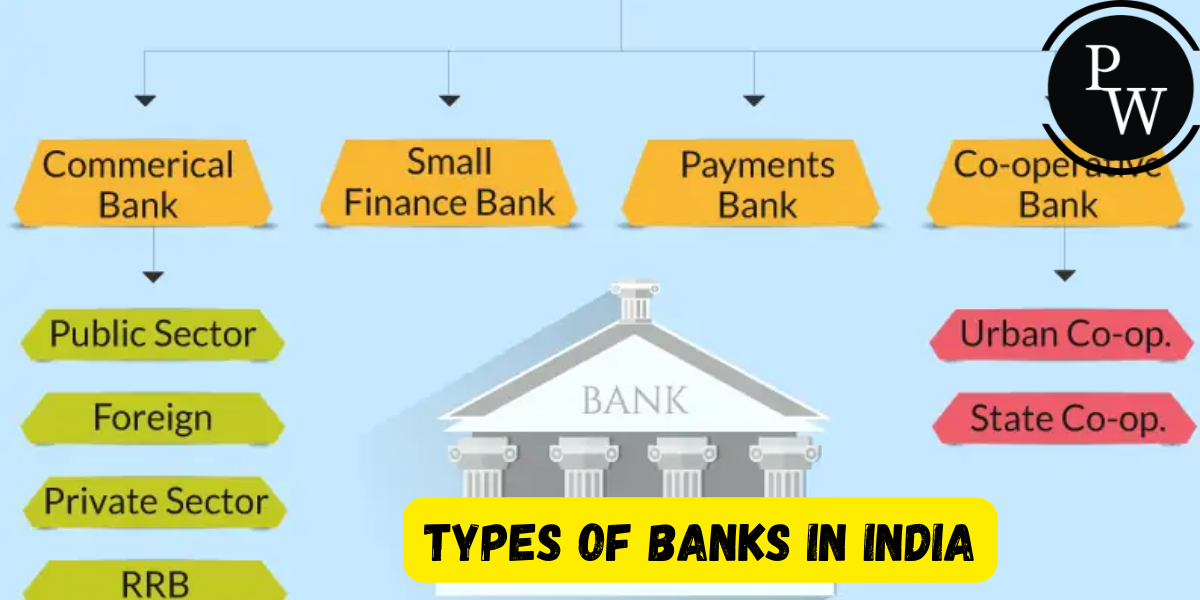

Banks are not all the same. Some are owned by the government. Some are owned by private companies. Others serve only villages or small businesses. In this guide, we break down every major type of bank here, so you never mix them up again.

Types of Banks in India Overview

Before we go deep into each category, here is a simple table that shows the different types of banks in India at a glance.

|

Type of Bank |

Who Owns It |

Main Purpose |

Example |

|

Public Sector Banks |

Government of India (majority stake) |

General banking, financial inclusion |

State Bank of India |

|

Private Sector Banks |

Private companies or individuals |

General banking, retail and digital services |

HDFC Bank |

|

Regional Rural Banks (RRBs) |

Central Government, State Government, and a sponsor bank |

Rural credit and farm loans |

Baroda UP Bank |

|

Co-operative Banks |

Members of the co-operative society |

Local savings and credit needs |

Urban Co-operative Banks |

|

Small Finance Banks (SFBs) |

RBI-licensed private promoters |

Loans to small businesses and farmers |

AU Small Finance Bank |

|

Payment Banks |

RBI-licensed private promoters |

Deposits and digital payments only |

India Post Payments Bank |

This table gives you a bird's-eye view. Now let's look at each type of bank one by one.

Public Sector Banks (PSBs) in India

Public sector banks are banks in which the Government of India owns a majority stake. This means the Government of India has more than 51% ownership in these banks. Public sector banks were formed after the government took over several private banks in 1969 and 1980, in a move called nationalisation.

Following several mergers, India currently has 12 public sector banks. Some well-known names include State Bank of India, Punjab National Bank, Bank of Baroda, Canara Bank, and Union Bank of India. These banks focus on serving common people, farmers, and small businesses across the country, including remote areas.

Public sector banks are known for being safe and stable, since the government backs them. They also lead many government schemes, such as Jan Dhan accounts and priority sector lending to agriculture and small industries.

Names of all 12 Public Sector Banks in India:

|

S.No. |

Bank Name |

|

1 |

State Bank of India (SBI) |

|

2 |

Punjab National Bank |

|

3 |

Bank of Baroda |

|

4 |

Canara Bank |

|

5 |

Union Bank of India |

|

6 |

Bank of India |

|

7 |

Indian Bank |

|

8 |

Central Bank of India |

|

9 |

Indian Overseas Bank |

|

10 |

UCO Bank |

|

11 |

Bank of Maharashtra |

|

12 |

Punjab & Sind Bank |

Private Sector Banks in India

Private sector banks are owned mostly by private companies or individuals, not the government. They are regulated by the Reserve Bank of India (RBI), like all other banks in the country.

There are currently around 21 private sector banks operating in India. Popular examples are HDFC Bank, ICICI Bank, Axis Bank, and Kotak Mahindra Bank. These banks are famous for their fast digital services, modern apps, and quick customer support.

Private sector banks compete hard for customers, so they often bring new technology first, such as mobile banking, instant loans, and better mobile apps. This makes them popular with students and young professionals who want quick, easy banking.

Names of all 21 Private Sector Banks in India:

|

S.No. |

Bank Name |

S.No. |

Bank Name |

|

1 |

HDFC Bank |

12 |

IndusInd Bank |

|

2 |

ICICI Bank |

13 |

Jammu & Kashmir Bank |

|

3 |

Axis Bank |

14 |

Karnataka Bank |

|

4 |

Kotak Mahindra Bank |

15 |

Karur Vysya Bank |

|

5 |

Bandhan Bank |

16 |

Nainital Bank |

|

6 |

CSB Bank |

17 |

RBL Bank |

|

7 |

City Union Bank |

18 |

South Indian Bank |

|

8 |

DCB Bank |

19 |

Tamilnad Mercantile Bank |

|

9 |

Dhanlaxmi Bank |

20 |

YES Bank |

|

10 |

Federal Bank |

21 |

IDFC FIRST Bank |

|

11 |

IDBI Bank |

Regional Rural Banks (RRBs)

Regional Rural Banks, or RRBs, were set up in 1976 under the Regional Rural Banks Act. Their main goal is to give banking and credit facilities to farmers, farm labourers, and small businesses in rural areas.

RRBs are jointly owned by the Central Government, the concerned State Government, and a sponsor bank, which is usually a public sector bank. Over the years, many RRBs have been merged to make them stronger and more efficient. As of today, approximately 28 Regional Rural Banks (RRBs) operate in India, a number that keeps changing due to fresh mergers aimed at improving their reach and viability.

RRBs mainly work in the area assigned to them by the government. So, unlike public or private sector banks, they cannot open branches anywhere they wish. Their focus stays firmly on rural development and agricultural credit.

Names of some major Regional Rural Banks (RRBs) in India, with their sponsor bank:

|

RRB Name |

Sponsor Bank |

State(s) Covered |

|

Baroda UP Bank |

Bank of Baroda |

Uttar Pradesh |

|

Prathama UP Gramin Bank |

Punjab National Bank |

Uttar Pradesh |

|

Punjab Gramin Bank |

Punjab National Bank |

Punjab |

|

Uttar Bihar Gramin Bank |

Central Bank of India |

Bihar |

|

Kerala Gramin Bank |

Canara Bank |

Kerala |

|

Karnataka Gramin Bank |

Canara Bank |

Karnataka |

|

Chhattisgarh Rajya Gramin Bank |

Central Bank of India |

Chhattisgarh |

|

Rajasthan Marudhara Gramin Bank |

State Bank of India |

Rajasthan |

|

Andhra Pradesh Grameena Vikas Bank |

State Bank of India |

Andhra Pradesh |

|

Telangana Grameena Bank |

State Bank of India |

Telangana |

Note: India has around 28 RRBs at present, and this number keeps changing as the government continues to merge smaller RRBs into larger, stronger ones.

Co-operative Banks in India

Co-operative banks work a little differently from the other types of banks in India. They are formed and owned by their members under the Co-operative Societies Act, 1912. Their primary objective is to serve their members rather than maximise profits.

Co-operative banks are of two broad kinds:

-

Urban Co-operative Banks (UCBs): These serve people living in cities and towns, mostly small traders and salaried employees.

-

Rural Co-operative Banks: These serve farmers and rural communities, offering short-term and long-term agricultural credit.

Co-operative banks are regulated jointly by the RBI and the National Bank for Agriculture and Rural Development (NABARD). In recent years, the RBI has strengthened its supervision of urban co-operative banks to keep an eye on their loan quality and financial health, since some smaller co-operative banks have faced stress in the past.

Names of some well-known Co-operative Banks in India:

|

Co-operative Bank Name |

Type |

Headquarters |

|

Saraswat Co-operative Bank |

Urban Co-operative Bank |

Mumbai, Maharashtra |

|

SVC Co-operative Bank |

Urban Co-operative Bank |

Mumbai, Maharashtra |

|

Cosmos Co-operative Bank |

Urban Co-operative Bank |

Pune, Maharashtra |

|

NKGSB Co-operative Bank |

Urban Co-operative Bank |

Mumbai, Maharashtra |

|

Abhyudaya Co-operative Bank |

Urban Co-operative Bank |

Mumbai, Maharashtra |

|

Bharat Co-operative Bank |

Urban Co-operative Bank |

Mumbai, Maharashtra |

|

State Co-operative Banks |

Rural Co-operative Bank (apex level) |

State capitals |

|

District Central Co-operative Banks |

Rural Co-operative Bank (district level) |

District headquarters |

|

Primary Agricultural Credit Societies (PACS) |

Rural Co-operative Bank (village level) |

Villages across India |

Small Finance Banks (SFBs)

Small finance banks are a newer addition to the banking system in India. The RBI created this category to help small business owners, marginal farmers, and micro-enterprises who often find it hard to get loans from bigger banks.

Small finance banks are licensed under the Banking Regulation Act, 1949, and there are around 12 of them functioning in India today. Examples include AU Small Finance Bank, Equitas Small Finance Bank, and Jana Small Finance Bank.

Unlike payment banks, small finance banks can do almost everything a normal bank does. They can accept deposits and also give out loans. Their special focus, though, remains on people and businesses that are underserved by traditional commercial banks.

Payment Banks

Payment banks are a special, limited type of bank. The RBI created them to boost financial inclusion and encourage digital payments across India, especially in areas with fewer bank branches.

Payment banks can accept deposits, but only up to a certain limit per customer. They cannot provide loans or issue credit cards. Their job is mainly to handle savings, remittances, and digital transactions. Well-known examples include India Post Payments Bank and Airtel Payments Bank.

Because they do not lend money, payment banks carry lower risk. They mostly earn through transaction fees and small deposit-based services, making them useful for quick, everyday digital banking needs.

Commercial Banks Vs Scheduled Banks

Students often get confused between "commercial banks" and "scheduled banks." Here is the simple difference:

-

Commercial banks are a broad category. It includes public sector banks, private sector banks, foreign banks, regional rural banks, small finance banks, and payment banks. Most commercial banks accept deposits and provide loans, although payment banks only accept deposits and facilitate digital payment services.

-

Scheduled banks are banks listed in the Second Schedule of the RBI Act, 1934. To become a scheduled bank, an institution must meet certain rules, such as having a minimum paid-up capital. Most commercial banks in India, including PSBs, private banks, RRBs, and SFBs, are scheduled banks.

So, almost every major type of bank you read about above already falls under the wider banking system in India that the RBI supervises and regulates.

Types of Banks in India FAQs

How many types of banks are there in India?

What is the main difference between public sector banks and private sector banks?

Can payment banks give loans to customers?

What is the purpose of Regional Rural Banks?

Who regulates all types of banks in India?