Difference Between Cash Flow and Income Statement

A cash flow statement details cash movements from operations, financing, and investments, while an income statement shows revenues, gains, expenses, and losses over time. Check difference between Cash Flow and Income Statement.

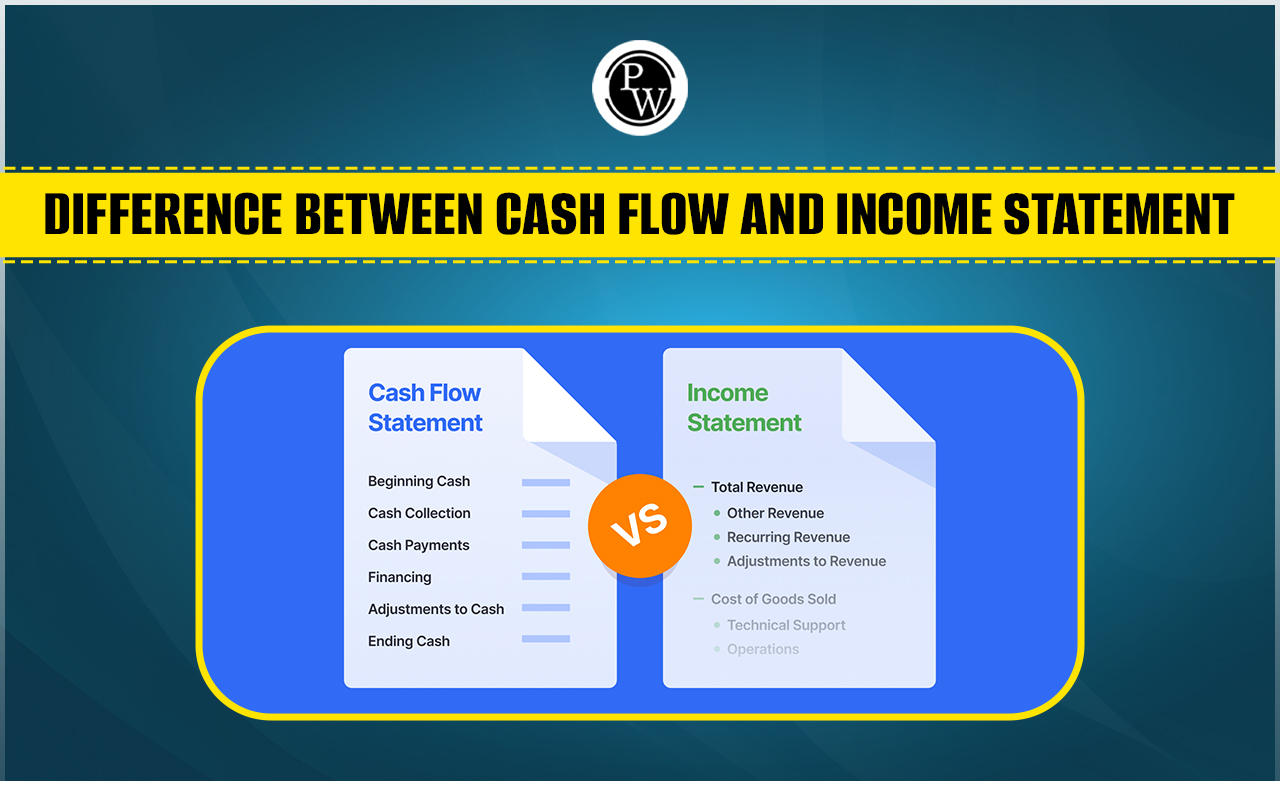

When studying finance, it's essential to understand the difference between Cash Flow and Income Statement. The Cash Flow Statement shows how cash moves in and out of a business, covering its operating, financing, and investing activities. For example, if a company receives ₹50,000 from a new loan, this inflow is recorded in the financing section of the Cash Flow Statement.

On the other hand, the Income Statement summarises a company's revenues and expenses over a specific period, showing how much profit or loss the business has made. For instance, if the same company earned ₹1,00,000 in sales but had ₹60,000 in expenses, the Income Statement would reflect a profit of ₹40,000. Understanding these financial statements is crucial for Commerce Students as it helps them assess a company’s financial health. While the Cash Flow Statement focuses on the actual movement of cash, the Income Statement highlights overall profitability. For more detailed information and examples, students can learn everything about the difference between a Cash Flow Statement and an Income Statement.Cash Flow Statement Meaning

The Cash Flow Statement is a financial record depicting the total amount of cash flowing into and out of a business over a given period. Its primary purpose is to provide insight into the company's liquidity and solvency, meaning how well the business can generate cash to meet its debts and cover operating expenses. Every company prepares a Cash Flow Statement at the end of the financial year to understand its cash position. The statement is divided into three major components:1. Cash Flow from Operating Activities

This section covers the cash generated from the company’s core business activities, like selling products or providing services. It includes cash inflows and outflows related to revenue, rent, salaries, and interest payments. For example, if a business earns money from selling its products, this would be recorded here. The Cash Flow from Operating Activities can be calculated using either the direct or indirect method.2. Cash Flow from Investing Activities:

This part focuses on cash flow resulting from the purchase or sale of assets and investments, as well as income from interest, dividends, or rent. For instance, if a company buys new equipment or sells an old one, the related cash flow would be recorded in this section.3. Cash Flow from Financing Activities:

This section reflects the cash that comes from funding activities, such as issuing shares, borrowing money, or repaying debts. It also includes cash outflows like interest payments, dividends to shareholders, or repurchasing stock. The Cash Flow Statement is vital for assessing a company's ability to generate enough cash to maintain operations and grow.Income Statement Meaning

The Income Statement is one of the most crucial financial documents a company prepares. It provides a clear picture of whether a business has made a profit or incurred a loss over a specific accounting year. This statement is created by first calculating the total revenue the company has earned and then subtracting all the expenses, including costs related to both operating (like salaries and rent) and non-operating activities (like taxes and interest). Many companies view the Income Statement as essential because it gives stakeholders, such as investors and management, a detailed understanding of the company's financial performance. Key items included in this statement are gross profit, net profit, total revenue, and various expenses. This document serves as the foundation for preparing a company’s overall financial report, as it contains most of the necessary financial data. Also Read: Class 12 Accountancy 2024, Important Topics, Marks Weightage, TipsDifference between Cash Flow Statement and Income Statement

Both the Cash Flow Statement and Income Statement are essential for stakeholders to get a comprehensive view of a company’s financial position and performance. Understanding the difference between Cash Flow and Income Statements helps businesses identify the right steps to ensure long-term success. While both statements provide valuable insights, they focus on different aspects of a business’s financial performance. Below is a detailed comparison of the two, including examples to make these concepts easier to grasp:| Difference Between Cash Flow and Income Statement | ||

| Aspects | Cash Flow Statement | Income Statement |

| Definition | Cash Flow Statement tracks all cash coming in and going out of the business during a specific time period. | Income Statement records all income, expenses, gains, and losses over a specific time period. |

| Focus | Highlights the company’s liquidity and cash management. | Highlights the company’s profitability. |

| How It's Recorded | Uses the actual cash received and paid out. | Uses income and expenses that may not have been received or paid yet. |

| Categories |

Divided into:

|

Divided into:

|

| Purpose | Shows how well a business can manage its cash to pay off debts and cover expenses. | Shows if a business is making a profit or loss. |

| How It's Created | It is based on the Income Statement and Balance Sheet. | It is based on various ledger accounts and financial records. |

| Depreciation | Does not include depreciation since it doesn't involve actual cash. | Includes depreciation as part of the expenses. |

| Timing of Reporting | Reflects cash movements when they occur. | Reflects income and expenses when they are earned or incurred, not necessarily when cash is exchanged. |

| Reporting Frequency | Often prepared quarterly or annually to assess short-term cash positions. | Typically prepared monthly, quarterly, or annually to evaluate ongoing profitability. |

| Example | If a company pays for new machinery, the actual payment is recorded in the Cash Flow Statement. | If a company earns revenue from a sale but hasn’t received the payment yet, it’s recorded in the Income Statement as income. |

Also Read: What is the Difference Between Balance Sheet and Cash Flow Statement?

The difference between Cash Flow Statement and Income Statement is essential for evaluating a company’s financial status. The Cash Flow Statement shows actual cash movements, while the Income Statement focuses on profitability by tracking income and expenses. Together, they provide a comprehensive view of a company’s financial performance. Therefore, Physics Wallah (PW) is the top choice for Commerce students, offering expert guidance and a deep understanding of complex financial concepts. PW’s dedicated approach helps students excel academically and professionally in the field of commerce. Join Now for the PW Commerce Online Course to master financial concepts and boost your career prospects with expert guidance and comprehensive training!| Also Check: | |

| Balance Sheet | Monopoly |

| Speculation | Network Marketing |

| Maslow’s Hierarchy of Needs | Development Of Indian Accounting Standards |

Difference Between Cash Flow and Income Statement FAQs

Why is cash flow more important than the income statement?

Cash flow better reflects your business's current financial health. Calculated monthly, it shows whether more cash is entering (positive) or leaving (negative) the business, giving a clear picture of liquidity.

What is the main difference between cash flow and income statement?

A cash flow statement shows actual cash inflows and outflows over time, while an income statement details revenues and expenses, including non-cash items like depreciation, to measure profitability during the same period.

What are the three types of cash flow statements?

Cash flow statements are divided into three categories: operating activities, investing activities, and financing activities. Each section provides insights into different aspects of a business's cash management.

What is the cash flow formula?

The formula for operating cash flow is: Operating Cash Flow = Operating Income + Depreciation – Taxes + Change in Working Capital. This formula shows how much cash your business generates from its operations.

What is the formula for the income statement?

The income statement formula involves three steps: calculating gross profit by subtracting the cost of goods sold from net sales, determining operating income by subtracting operating expenses from gross profit, and finally, finding net income by adding non-operating income.

🔥 Trending Blogs

Talk to a counsellorHave doubts? Our support team will be happy to assist you!

Join 15 Million students on the app today!

Free Learning Resources

PW Books

Notes (Class 10-12)

PW Study Materials

Notes (Class 6-9)

Ncert Solutions

Govt Exams

Our Other Websites

Class 6th to 12th Online Courses

Govt Job Exams Courses

UPSC Coaching

Defence Exam Coaching

Gate Exam Coaching

Other Exams

Know about Physics Wallah

Physics Wallah is an Indian edtech platform that provides accessible & comprehensive learning experiences to students from Class 6th to postgraduate level. We also provide extensive NCERT solutions, sample paper, NEET, JEE Mains, BITSAT previous year papers & more such resources to students. Physics Wallah also caters to over 3.5 million registered students and over 78 lakh+ Youtube subscribers with 4.8 rating on its app.

We Stand Out because

We provide students with intensive courses with India’s qualified & experienced faculties & mentors. PW strives to make the learning experience comprehensive and accessible for students of all sections of society. We believe in empowering every single student who couldn't dream of a good career in engineering and medical field earlier.

Our Key Focus Areas

Physics Wallah's main focus is to make the learning experience as economical as possible for all students. With our affordable courses like Lakshya, Udaan and Arjuna and many others, we have been able to provide a platform for lakhs of aspirants. From providing Chemistry, Maths, Physics formula to giving e-books of eminent authors like RD Sharma, RS Aggarwal and Lakhmir Singh, PW focuses on every single student's need for preparation.

What Makes Us Different

Physics Wallah strives to develop a comprehensive pedagogical structure for students, where they get a state-of-the-art learning experience with study material and resources. Apart from catering students preparing for JEE Mains and NEET, PW also provides study material for each state board like Uttar Pradesh, Bihar, and others

Copyright © 2026 Physicswallah Limited All rights reserved.