Accounting for Debentures, Kinds, Issue, Methods

Accounting for Debentures: The word ‘debenture’ has been derived from the Latin word ‘debere’ which means to borrow. A debenture is a written document, kind of like a contract, that a company makes when it borrows money. It promises to pay back the borrowed money after a certain time or in regular instalments.

Also, it promises to pay interest at a fixed rate, usually every six months or once a year, on specific dates. Debentures are a type of loan that a company takes, and the company has to pay interest on them regardless of whether it makes a profit or not. In this article, learn more about debentures for CS Exams .What is Debenture in Accounting Terms?

Accounting for Debentures is a marketable security that businesses can issue to obtain long-term financing without needing to put up collateral or dilute their equity. A debenture is a type of long-term business debt not secured by any collateral. It is a funding option for companies with solid finances that want to avoid issuing shares and diluting their equity. Debentures can also be useful for companies that don’t want to tie up assets or who lack collateral for a traditional loan.Kinds of Debentures

Secured or Mortgage: When debentures are secured by a mortgage or charge on the property of the company, they are called secured or mortgage debentures.

Unsecured or Naked: When debentures are issued without any security, they are termed as unsecured or naked debentures.

Bearer: These debentures are payable to the bearer and are transferable by mere delivery. Interest coupons are attached to each debenture. The interest and principal amount on such debentures is payable upon presentation and delivery of coupons and debentures.

Registered Debenture: Interest and principal amount is paid only to the person whose name is registered in the debenture ledger. Such debentures are transferable through a transfer deed.

Convertible: Debentures may be convertible into preference or equity shares of the company on certain specified dates based on an agreement between the company and the debenture holders.

Non-Convertible: Such debentures are paid in cash.

Redeemable Debenture: Such debentures are paid either at par or at a premium after the expiry of a particular period or under a system of periodical drawings.

Irredeemable or Perpetual Debenture: Such debentures are payable either on a happening of the contingency, when the company winds its business up, or when the company decides to redeem itself.

First Mortgage Debentures: Such debentures are paid based on priority as compared to other debentures.

Second Mortgage Debentures: Such debentures are paid after the redemption of the first mortgage debentures.

Difference between Shares and Debentures

Check the differences between shares and debentures in the table below:| Difference between Shares and Debentures | ||

| Points | Shares | Debentures |

| Ownership | A ‘share’ represents ownership of the company. A share is a part of the owned capital. | A ‘debenture’ is only acknowledgement of Debt. A debenture is a part of borrowed capital. |

| Return | The return on shares is known as dividend. The rate of return on shares may vary from year to year depending upon the profits of the company. | The return on debentures is called interest. The rate of interest on debentures is prefixed. |

| Repayment | Normally, the amount of shares is not returned during the life of the company. | Generally, the debentures are issued for a specified period and repayable on the expiry of that period |

| Voting Rights | Shareholders enjoy voting rights. | Debenture holders do not normally enjoy any voting right. |

| Security | Shares are not secured by any charge. | Debentures are generally secured and carry a fixed or floating charge over the assets of the company. |

| Convertibility | Shares cannot be converted into debentures. | Debentures can be converted into shares if the terms of issue so provide, and in that case these are known as convertible debentures. |

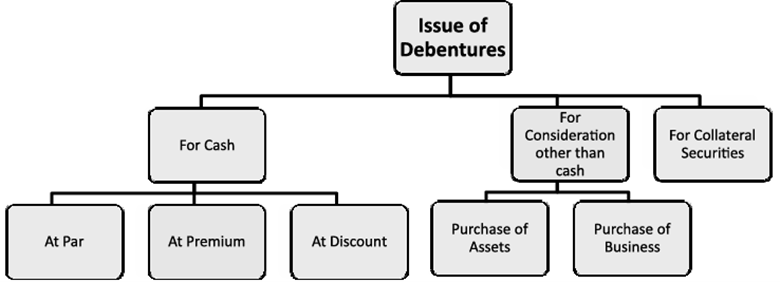

Issue of Debentures

Conditions for issue of debentures as per Companies Act, 2013

- Issue of Debentures by Special Resolution

- No Voting Rights

- Terms for the Issue of Secured Debentures

- Creation and Utilization of Debenture Redemption Reserve

- Debenture Trustee(s) to protect the interest of debenture holder

Debenture Interest

When a company issues debentures, it commits to paying interest at a fixed rate, like 8% or 10%, mentioned in the debenture name. This interest, calculated on the debenture's face value, must be paid half-yearly. It's a company expense, payable even if the company hasn't made a profit.Terms of Issue of Debentures

- Issued at par and redeemable at par

- Issued at a discount and redeemable at par

- Issued at a premium and redeemable at par

- Issued at par and redeemable at a premium

- Issued at a discount and redeemable at a premium

- Issued at a premium and redeemable at a premium

Accounting Treatment of Discount/Loss on the Issue of Debentures

The discount or loss on debentures, being a capital loss, should be written off over the debentures' lifetime. It cannot be fully written off in the year of issue because the benefit lasts until redemption. There are two options:- Write off against capital profits.

- Treat as deferred revenue expenditure and write off over the debentures' lifetime.

Fixed Installment Method: Where the debentures are redeemable at the end of a specific period, the total amount of discount should be written off in equal instalments of a fixed amount over that period.

Fluctuating Installment Method: If the debentures are to be repaid by annual drawings or instalments it would be equitable in such a case to write off a discount in proportion to the unpaid amount of debentures.

Redemption of Debentures

Redemption of debentures means paying off the debenture amount by the company according to the terms of the issue. In simple terms, it's when the company repays the debenture holders.Creation of Debenture Redemption Reserve (DRR)

Under Section 71(4) of the Companies Act, 2013, and Rule 18(7) of the Companies (Share Capital And Debentures) Rules, 2014, companies issuing redeemable non-convertible debentures must create a Debenture Redemption Reserve (DRR) from their profits. This reserve, a percentage of the debenture value, ensures funds are available exclusively for debenture repayment, protecting debenture holders from potential defaults.Investment of Debenture Redemption Reserve (DRR) Amount

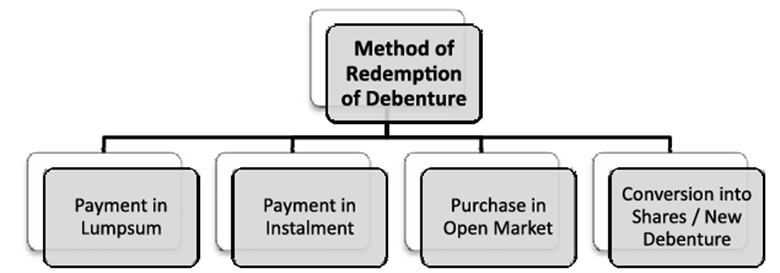

As per Rule 18 (7) of the Companies (Share Capital and Debentures) Amendment Rules, 2019, the following companies: (a) All listed NBFCs (b) All listed HFCs (c) All other listed companies (other than AlFIs, Banking Companies and Other FIs); and (d) All unlisted companies which are not NBFCs and HFCs shall on or before the 30th day of April in each year, in respect of debentures issued, deposit or invest, as the case may be, a sum which should not be less than 15% of the amount of its debentures maturing during the year ending on the 31st day of March of next year, in any one or more of the following methods, namely: (a) in deposits with any scheduled bank, free from charge or lien; (b) in unencumbered securities of the Central Government or of any State Government; (c) in unencumbered securities mentioned in clauses (a) to (d) and (ee) of Section 20 of the Indian Trusts Act, 1882; (d) in unencumbered bonds issued by any other company which is notified under clause (f) of Section 20 of the Indian Trusts Act, 1882.Methods of Redemption of Debentures

Lumpsum: The redemption is made in one lumpsum at the expiry of a specified period promised as the redemption date when the debentures were issued.

Annual Installments or Draw by Lots: Under this method, a certain amount of debentures is redeemed at regular intervals, say yearly, during the life of debentures. The amount of annual drawings may or may not be equal.

Conversion into Shares: A company may issue convertible debentures, giving options to the debenture holders to exchange their debentures for equity shares or preference shares in the company.

Purchase of Its Debentures in the Open Market: A company is entitled to purchase its debentures in the open market, i.e., through the stock exchange. When the company purchases its debentures for immediate cancellation, it leads to automatic redemption. Own debentures may also be purchased by the company for its investment and the same may be reissued in future too.

Purchase of Debentures Before the Specified Date of Payment of Interest

Interest on debentures is usually paid every six months on specified dates like September 30th and March 31st. When debentures are bought on these dates, there's no problem as interest is paid to the holders. However, if debentures are bought before the interest payment date, it's unclear if the purchase price includes interest for the period from the last payment date to the purchase date. It's crucial to determine if the debenture price is quoted as "Cum-interest" or "Ex-interest" to understand if it includes interest for the past period. "Cum-interest" means the price includes past interest, while "Ex-interest" means it doesn't include past interest. Enhance your corporate expertise with PW Company Secretary Courses . Explore debentures and more for CS exam preparation. Enroll now for comprehensive learning and professional growth.| Also Check: | |

| Introduction to Accounting | Capital Structure |

| Introduction to Accounting Standards | Introduction to Corporate Accounting |

| Time Value of Money | Accounting for Share Capital |

Accounting for Debentures FAQs

What is a debenture?

What are the types of debentures?

How are debentures different from shares?

How is interest on debentures paid?

What are the methods of debenture redemption?