Profit Margin Formula: Definition, Applications, Examples

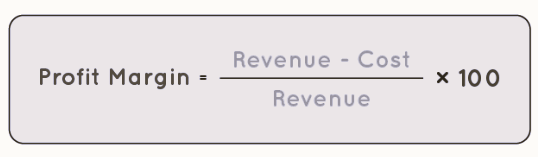

The Profit Margin Formula is a valuable tool for assessing the profitability of a sale or a business. It is a ratio that measures how efficiently a company operates and is expressed as a percentage. Profit margin is calculated by dividing the net profit, which is the income remaining after subtracting all expenses, including the cost of goods sold, raw material expenses, labor costs, and more, by the total revenue generated. The formula for profit margin is as follows:

What is the Profit Margin Formula?

The profit margin formula can be further divided into two key components: the Gross Profit Margin Formula and the Net Profit Margin Formula. These two formulas provide different perspectives on a company's profitability.

1. Gross Profit Margin Formula:

The gross profit margin formula focuses on the profitability of a company's core business operations, excluding operating expenses such as wages, utilities, and taxes. It is calculated as follows:

Gross Profit Margin (%) = [(Revenue - Cost of Goods Sold) / Revenue] × 100

Where:

Revenue represents the total income generated from sales or other sources.

Cost of Goods Sold (COGS) includes the direct costs associated with producing the goods or services sold, such as raw materials, labor, and manufacturing expenses.

A higher gross profit margin indicates that a company is effectively managing its production costs and generating a larger profit from its primary activities.

2. Net Profit Margin Formula:

The net profit margin formula provides a more comprehensive view of a company's overall profitability, as it takes into account all operating expenses, taxes, interest, and other costs. It is calculated as follows:

Net Profit Margin (%) = (Net Profit / Revenue) × 100

Where:

Net Profit is the total profit remaining after deducting all expenses, including the cost of goods sold, operating expenses, taxes, interest, and other costs.

Revenue represents the total income generated from sales or other sources.

A higher net profit margin indicates that a company is efficiently managing both its core operations and its overall financial responsibilities.

These two profit margin formulas are valuable for assessing different aspects of a company's financial performance. The gross profit margin focuses on the efficiency of production, while the net profit margin offers a broader view of the company's financial health by considering all operating and financial factors.

Profit Margin Formula Applications

The profit margin formula has various practical applications in business and finance. It is a fundamental financial metric that helps assess the profitability of a company or a specific product or service. Here are some of the key applications of the profit margin formula:

- Financial Analysis: Profit margin analysis is crucial for financial analysts, investors, and stakeholders when evaluating the financial health of a company. It helps in understanding how efficiently a company is generating profits from its operations.

- Comparative Analysis: Profit margins are often used to compare the financial performance of different companies within the same industry. Investors and analysts can use this data to identify industry leaders and laggards.

- Investment Decision-Making: Investors use profit margin data to make investment decisions. A company with a higher profit margin may be seen as a more attractive investment opportunity.

- Pricing Strategy: Businesses use profit margin analysis to set appropriate pricing for their products and services. Understanding profit margins helps determine the balance between generating revenue and covering expenses.

- Cost Control: Companies can use profit margin analysis to identify areas where they can reduce costs. By pinpointing expenses that are affecting profit margins, they can implement cost-saving measures.

- Product Analysis: Businesses can assess the profitability of individual products or product lines. This can help in determining which products are most profitable and which may need adjustment or discontinuation.

- Performance Evaluation: Managers and executives use profit margin data to evaluate the performance of different departments or business units within a company. It helps in identifying areas that need improvement.

- Risk Assessment: Understanding profit margins can help companies assess financial risk. A narrow profit margin may make a business more vulnerable to economic downturns or unforeseen expenses.

- Creditworthiness Evaluation: Lenders and financial institutions often consider a company's profit margin when assessing its creditworthiness. A healthy profit margin may lead to better borrowing terms.

- Business Planning: Companies use profit margin analysis as a part of their strategic planning. It helps in setting financial goals and developing strategies to achieve those goals.

Profit Margin Formula Examples

Example 1: Gross Profit Margin

Suppose a retail store generated $500,000 in revenue and incurred $300,000 in costs related to purchasing goods for resale (Cost of Goods Sold or COGS). To calculate the gross profit margin:

Gross Profit Margin (%) = [(Revenue - COGS) / Revenue] × 100

Gross Profit Margin (%) = [(500,000 - 300,000) / 500,000] × 100

Gross Profit Margin (%) = (200,000 / 500,000) × 100

Gross Profit Margin (%) = 40%

So, the gross profit margin for this retail store is 40%. This indicates that 40% of the revenue is retained after accounting for the cost of goods sold.

Example 2: Net Profit Margin

Let's consider a software company that reported $1,000,000 in revenue. After accounting for various expenses, the net profit was $250,000. To find the net profit margin:

Net Profit Margin (%) = (Net Profit / Revenue) × 100

Net Profit Margin (%) = (250,000 / 1,000,000) × 100

Net Profit Margin (%) = (1/4) × 100

Net Profit Margin (%) = 25%

The net profit margin for this software company is 25%. This means that after considering all expenses, the company retains 25% of its revenue as profit.

Example 3: Comparing Profit Margins

Let's compare two competing companies in the same industry. Company A has a revenue of $1,500,000 and a net profit of $300,000, while Company B has a revenue of $2,000,000 and a net profit of $400,000.

Company A's Net Profit Margin (%) = (300,000 / 1,500,000) × 100 = 20%

Company B's Net Profit Margin (%) = (400,000 / 2,000,000) × 100 = 20%

Both companies have a net profit margin of 20%, indicating that they retain the same percentage of profit relative to their respective revenues. This comparison helps assess their relative profitability.

Example 4: Cost Reduction Impact on Profit Margin

Suppose a manufacturing company with $1,000,000 in revenue has a net profit of $100,000. The company identifies cost-saving opportunities and reduces its expenses to $80,000 while keeping revenue constant. To calculate the impact on the net profit margin:

Initial Net Profit Margin (%) = (100,000 / 1,000,000) × 100 = 10%

New Net Profit Margin (%) = (100,000 - 20,000) / 1,000,000 × 100 = 8%

The cost reduction has increased the net profit margin from 10% to 8%, indicating improved profitability due to lower expenses.

These examples demonstrate how the profit margin formula can be used to assess and compare the profitability of businesses and to evaluate the impact of cost changes on profit margins.

| Related Links | |

| Data Handling Formula | Logarithm Formula |

| Introduction to Graph Formula | Factorial Formula |

Profit Margin Formula FAQs

Q1. What is the profit margin formula used for?

Q2. What are the common types of profit margin?

Q3. How do I calculate the gross profit margin?

Q4. How do I calculate the net profit margin?

Q5. What is a good profit margin?