How Credit Score Works in India?

How Credit Score Works in India?

The credit score, a determinant of an individual's ability to repay debt based on their credit history, plays a pivotal role in modern banking systems. Financial institutions rely on credit scores to assess whether an applicant qualifies for a loan, and this extends to pre-approved loan offers targeted at prospective consumers.

Authorized companies analyze credit scores based on an individual's past financial transactions. These firms, licensed by the Reserve Bank of India, collaborate with financial institutions to obtain comprehensive information about applicants, a process known as checking the credit score.

What is a Credit Score?

A credit score, a three-digit numerical representation, is utilized by banks to ascertain the eligibility of a potential borrower for a loan or credit card. Credit bureaus analyze your detailed credit history, outlined in your credit report, to derive this score. Although each credit agency uses a distinct formula to calculate credit scores, the underlying variables considered are consistent.

Also Read: Credit Bureaus in India

Credit Rating Companies in India

In India, four authorized companies, licensed by the Reserve Bank of India, provide credit reports and ratings:

- TransUnion CIBIL: Widely known as CIBIL, it is an American multinational with extensive popularity in India due to widespread partnerships with financial institutions.

- Equifax: A collaborative venture between American and Indian companies, Equifax India presents data in a user-friendly manner.

- Experian: An international credit bureau headquartered in Ireland, Experian provides credit scores similar to other bureaus in India, offering free scores on WhatsApp.

- CRIF Highmark: A purely Indian company, CRIF boasts the world's largest microfinance credit database.

How to Obtain Credit Ratings?

All four bureaus provide individuals with their credit scores for free once a year. Various websites also offer this service. Individuals can log into the bureau's websites and request their credit scores by providing details such as Aadhar card and PAN number. Experian even allows users to obtain their credit score for free via WhatsApp without any restrictions on the frequency of requests.

How to Calculate Credit Score?

Credit bureaus employ diverse algorithms to calculate credit scores. In India, the major credit bureaus are CIBIL, Experian, Equifax, and CRIF High Mark, each employing unique scoring models. Consequently, credit scores may vary across bureaus. Another contributing factor to score discrepancies is that financial activities may not be reported to all bureaus by lenders, impacting score calculations.

Common factors considered for credit score calculation include:

- Payment History: Encompassing credit cards, personal loans, and other financial obligations, your payment history reflects timely payments, late payments, and bankruptcies.

- Credit Utilization Ratio: This ratio, indicating the proportion of used credit to available credit, significantly influences credit scores. A ratio exceeding 30% can negatively impact the score.

- Total Number of Accounts: The variety of credit products in your portfolio, such as home loans and credit cards, contributes positively to your credit score.

- Age of Credit: The longer your credit history, the better for your score. Keeping old accounts open, even after paying off debts, is advisable.

However, the impact of these factors on credit score calculation varies. Payment history and credit utilization ratio have high impacts, while the age of credit has a medium impact, and the total number of accounts has a low impact.

Factors not considered in credit score calculation include personal details such as age, salary, or employment tenure. Lenders may use this additional information when evaluating loan or credit card applications.

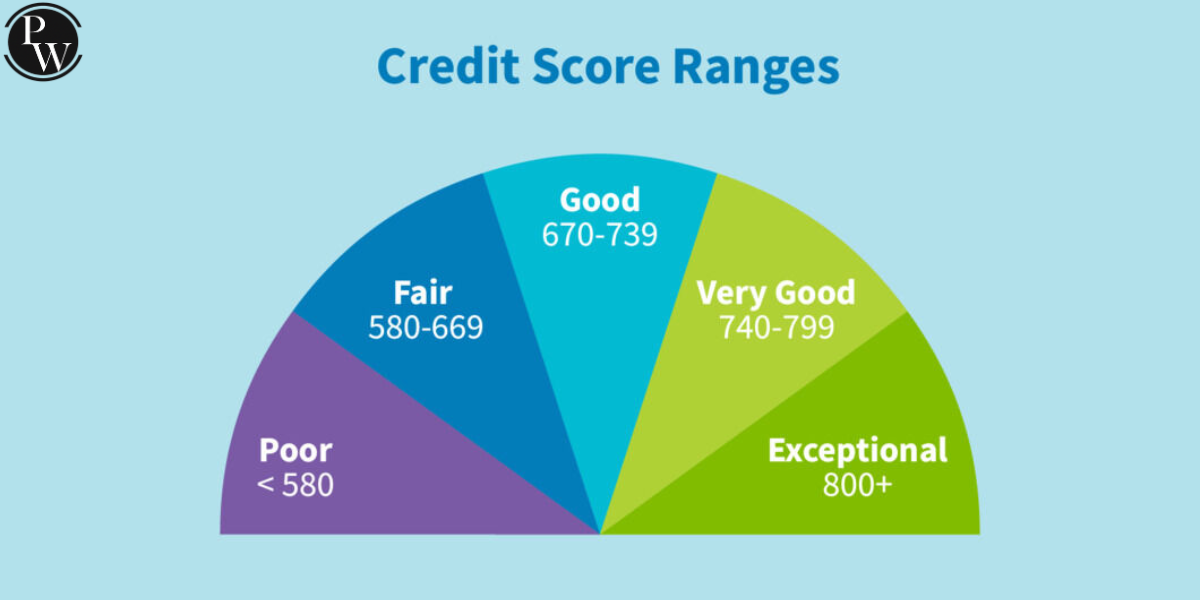

Credit Score Ranges for CIBIL

A credit score typically ranges from 300 to 900, though slight variations may exist. The CIBIL score range categorizes borrowers as follows:

| Credit Score Range | Rating |

|---|---|

| 300-499 | Poor |

| 500-649 | Average |

| 650-749 | Good |

| 750-900 | Excellent |

A generally accepted "good" credit score is 750 or higher, but specific lending institutions may have varying criteria. Regularly monitoring your credit report and maintaining a good credit score is crucial. Scores between 500 and 649 face difficulties in obtaining loans and may experience higher interest rates, but credit cards are still accessible. Scores below 500 face challenges in securing loans or credit cards.

Credit Score Ranges for Other Bureaus in India

Credit score ranges vary slightly among companies, but the rating categories remain consistent. Equifax, Experian, and CRIF Highmark each have their own ranges:

| Credit Bureau | Credit Score Range | Rating Categories |

|---|---|---|

| Equifax | 280-559 | Poor |

| 560-659 | Fair | |

| 660-724 | Good | |

| 725-759 | Very Good | |

| 760-850 | Excellent | |

| Experian | 300-549 | Poor |

| 550-649 | Fair | |

| 650-749 | Good | |

| 750-799 | Very Good | |

| 800-850 | Excellent | |

| CRIF Highmark | 300-549 | Low |

| 550-649 | Medium | |

| 650-749 | High | |

| 750-900 | Excellent |

Factors Used to Calculate Credit Score

Licensed credit bureaus use financial data to calculate credit scores, considering factors such as:

- Active Credit Accounts (mortgages, credit cards, loans)

- Credit Agreements (mobile phone contracts, car finance)

- Payments to Buy Now Pay Later Services

- Recently Closed or Settled Credit Accounts

- Public Record Information (CCJs, bankruptcies, IVAs)

- Fraud-related Information (stolen identity, fraud identity)

- Inclusion in the Electoral Register

Understanding and monitoring these factors is crucial for individuals aiming to maintain or improve their credit scores.

How is credit score calculated in India?

What is a good credit score in India?

Who assigns your credit score in India?

What is the most popular credit score rating in India?