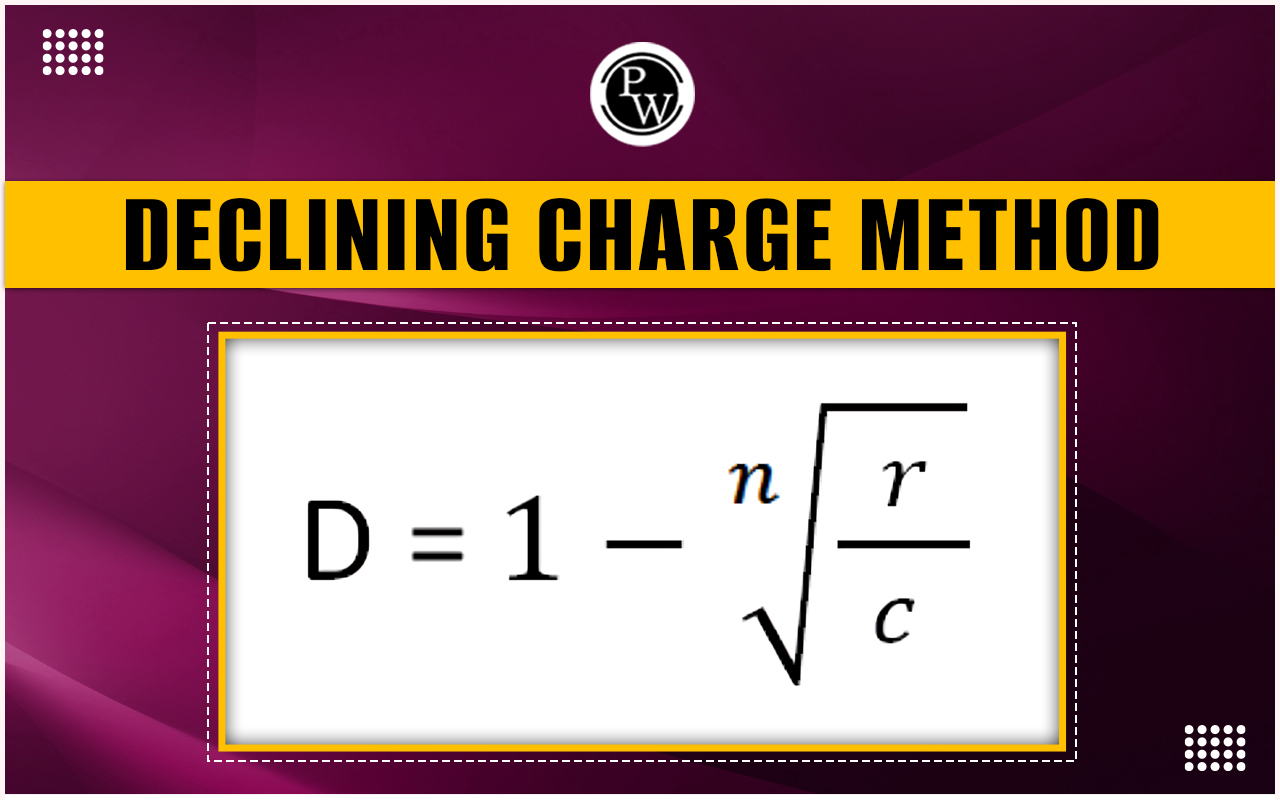

Declining Charge Method

The declining charge method, also known as the declining balance method, is a depreciation accounting technique that allocates a higher depreciation expense in the early years of an asset's life. This approach assumes that assets lose value more rapidly in their initial years of use, reflecting economic reality more closely than straight-line depreciation. By accelerating depreciation, businesses can more accurately reflect the wear and tear of assets over time. This method benefits companies seeking to align their financial statements with asset usage and value reduction. However, careful consideration of tax implications and the accuracy of financial reporting is required. Understanding and applying the declining charge effectively can enhance organisations' financial planning and management strategies.

What Is the Declining Charge Method?

The declining charge method, also known as the declining balance method, has been a popular approach in accounting for decades. It calculates the depreciation expense for fixed assets over their useful lives. Unlike the straight-line method, which spreads depreciation evenly across each year, the declining charge method assumes that an asset loses its value more rapidly in the earlier years of use and slows down in later years. For example, if a piece of equipment is purchased for $50,000 with a salvage value of $5,000 and a useful life of 5 years, and the depreciation rate is set at 30%, the depreciation expense for the first year would be $15,000 (30% of $50,000). In subsequent years, the depreciation expense would be calculated based on the reduced book value of the asset, which is the original cost minus the accumulated depreciation. This method is preferred for assets that experience greater wear and tear or technological obsolescence early in their life cycles. It provides a more accurate reflection of an asset’s decreasing value over time, aligning with matching expenses with revenues in financial reporting.Declining Charge Method

There are three primary methods used for charging depreciation, each designed to allocate the cost of an asset over its useful life:- Diminishing Balance Method : This approach applies a constant depreciation rate to the remaining book value of the asset each year. Depreciation expenses are higher in the earlier years and decrease as the asset's value declines.

- Sum of Years' Digits Method : This method considers the sum of the digits of an asset's useful life to calculate depreciation. It allocates more depreciation expense to earlier years, reflecting the asset's higher usage and wear during that period.

- Double Declining Method : Also known as the Double Declining Balance Method, this approach doubles the straight-line depreciation rate and applies it to the asset's book value. It accelerates depreciation expense in the initial years and is suitable for assets that rapidly lose value early in their useful life.

How to Calculate Declining Balance Depreciation

The depreciation rate is typically higher than the straight-line method, resulting in larger depreciation expenses in the earlier years of the asset's life and decreasing amounts in subsequent years. This approach is useful for assets that lose value more quickly in their early years. In this method, depreciation is applied as a percentage of the remaining book value of the asset each year. Where:- CBV = current book value of the asset

- DR = depreciation rate (%)

- Determine the Initial Cost : Start with the asset's initial cost, which includes any expenses incurred to acquire and prepare it for use, such as installation costs.

- Select the Depreciation Rate : Decide on the depreciation rate to use. The declining balance method typically uses a rate that is a multiple of the straight-line depreciation rate, often 1.5 times or 2 times the straight-line rate.

-

Calculate Annual Depreciation Expense

:

Begin with the asset's current book value (CBV) at the start of the accounting period.

- Multiply the CBV by the depreciation rate to find the annual depreciation expense.

- Annual Depreciation Expense = CBV×Depreciation Rat

- Update the Book Value : Subtract the annual depreciation expense from the CBV to get the new book value for the next accounting period.

New CBV= CBV−Annual Depreciation Expense

- Repeat Annually : Continue this process each year until the asset's book value is reduced to its salvage value or the end of its useful life.

Declining Balance Depreciation = CBV×DR

Advantages of the Declining Charge Method

The declining balance method of depreciation offers significant advantages for businesses and organizations managing their asset depreciation:- Front-Loaded Expense : It allows businesses to recognize higher depreciation expenses in the earlier years of an asset's life. This can align with the asset's actual usage and wear and tear, reflecting more accurately its decreasing economic benefits over time.

- Tax Benefits : In some tax jurisdictions, the declining balance method can result in higher depreciation deductions early on, lowering taxable income and reducing tax liabilities in those years.

- Asset Valuation : Since assets tend to depreciate more rapidly in their earlier years, the declining balance method can provide a more realistic view of an asset's current value on the balance sheet.

- Flexibility : Businesses can choose an appropriate depreciation rate based on the asset's expected useful life and the business's financial strategy. This flexibility allows for adjustments that better match depreciation expenses with revenue generation.

Disadvantages of Declining Charge Method

While advantageous in many respects, the declining balance method of depreciation also comes with some notable disadvantages.- Higher Initial Costs : Using the declining balance method front-loads depreciation expenses, resulting in higher expenses in the early years of an asset's life. This can negatively impact profitability and cash flow in the short term, especially if the business is still ramping up operations or facing financial constraints.

- Complexity in Calculation : Calculating depreciation under the declining balance method requires understanding and applying specific formulas and rates. This complexity can lead to errors in depreciation calculation, especially if the rates need to be accurately applied or if there are changes in accounting standards or asset usage patterns.

- Overstating Asset Value : Because declining balance depreciation results in higher depreciation expenses early on, it can lead to understating the remaining book value of the asset over time. This might not accurately reflect the asset's true economic or market value, which could affect financial ratios and decision-making.

- Regulatory and Reporting Challenges : Some regulatory bodies or accounting standards may restrict or discourage accelerated depreciation methods like declining balance. Compliance with these regulations and accurately reporting depreciation expenses may require additional effort and resources.

- Mismatch with Asset Usage : The declining balance method assumes a more rapid decline in an asset's value, which may not always align with its actual usage or economic obsolescence. This can lead to discrepancies between reported depreciation and the asset's economic life.

Begin your journey towards academic excellence in Commerce with our comprehensive Class 11 Commerce courses . Master the CBSE syllabus with expert guidance and ace your exams. Enroll now!”

Declining Charge Method FAQs

What is the method of depreciation charged?

What is the diminishing cost method?

Is depreciation charge a debit or credit?